If you have a 610 credit score, you may be wondering what that means. Is 610 a good credit score, a bad score, or somewhere in between? What does having a 610 credit score mean for your wallet? Read on to find out all you need to know about having a 610 credit score.

What is a 610 credit score?

The FICO Credit Score is the most widely known and used method for calculating your credit score. Although there are other versions, like the VantageScore, we’ll look at the FICO Score for the purpose of this article.

Your credit score is a three-digit number used to determine your creditworthiness. It typically ranges from 300 to 850, with the higher end being the better score. Your credit score is far more than just a number. It impacts everything from your ability to get approved for a credit card, mortgage or car loan to the amount of deposit you may have to put down for utility services, cell phones and more. In some cases, it can even influence whether or not you get hired for a new job.

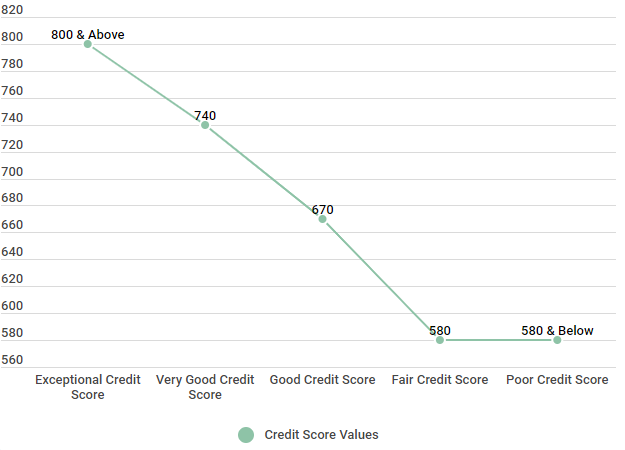

If you have a 610 credit score, you can see from the graph below why it is considered fair credit on the FICO score range.

FICO credit score ranges

| Credit Score Ranges | Credit Score Values |

|---|---|

| Exceptional Credit Score | 800 & Above |

| Very Good Credit Score | 740 - 799 |

| Good Credit Score | 670 - 739 |

| Fair Credit Score | 580 - 669 |

| Poor Credit Score | 580 & Below |

Source: Fair Isaac Corporation (myFICO.com).

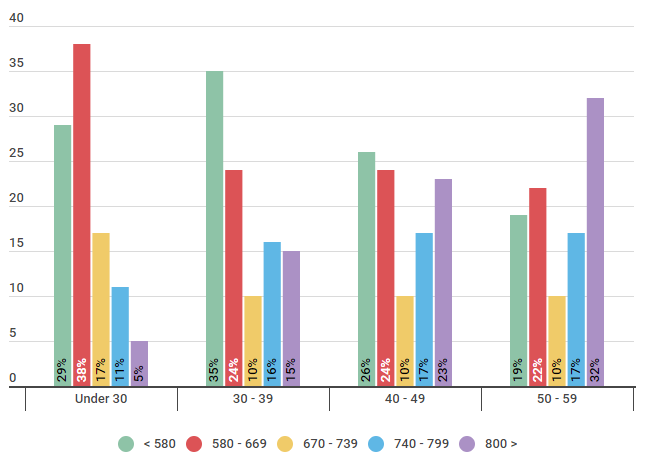

However, if you have a 610 credit score you’re not alone. Below you will find that 38 percent of the U.S. population under 30 has a similar credit score. In fact, 27 percent of the population have credit scores in this range.

U.S. Population Categorized by the Five FICO Ranges for Credit Scores

| Age | < 580 | 580 - 669 | 670 - 739 | 740 - 799 | 800 > |

|---|---|---|---|---|---|

| Under 30 | 29% | 38% | 17% | 11% | 5% |

| 30 - 39 | 35% | 24% | 10% | 16% | 15% |

| 40 - 49 | 26% | 24% | 10% | 17% | 23% |

| 50 - 59 | 19% | 22% | 10% | 17% | 32% |

Source: We ran a survey of 550 US consumers in different age groups on 9/26/2018 to understand which credit score ranges they fell into.

If you’re interested in improving your 610 credit score, there are smart strategies you can put in place to help you see significant changes.

How to improve your 610 credit score

Improving your 610 credit score doesn’t have to be difficult. In fact, there are several fairly easy ways to see an improvement in your score almost immediately.

- Apply for a secured credit card. A secured credit card is another great way to improve your credit. A secured credit card is easier to qualify for than a traditional credit card since it requires an up-front deposit. This deposit becomes your credit limit — so, if you default on your payments, the lender can simply take the funds out of your deposit.

- Apply for a credit building loan. Adding a credit building loan is a great way to not only build your credit history but to also diversify your credit portfolio. When you take out a credit building loan, a set amount of money is set aside for you in a special account. You continue to make payments until your loan is paid off — and then you have full access to the account.

These strategies can have a significant impact on credit score improvement.

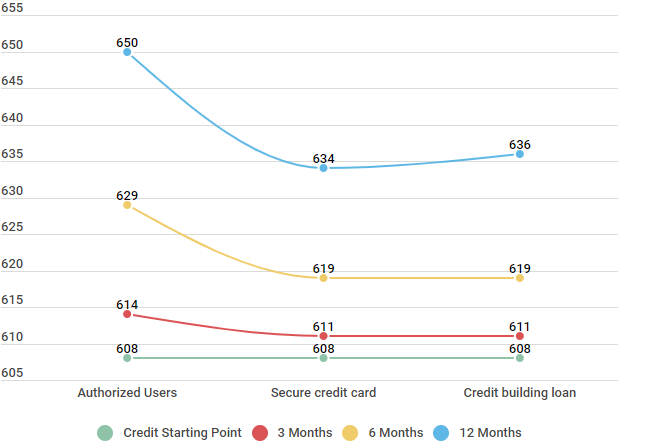

Average Credit Score Improvement starting with fair credit

| Method | Credit Starting Point | 3 Months | 6 Months | 12 Months |

|---|---|---|---|---|

| Secure credit card | 610 | 613 | 621 | 636 |

| Credit building loan | 610 | 613 | 621 | 638 |

Source: Review of 600 individuals increased their credit with different methods. The study was conducted in February of 2016 and concluded April of 2016.

Individuals who started with a 610 credit score were able to see a 3-point improvement in just 3 months by getting a secured credit card. Similarly, they also saw a 3-point improvement in just 3-months by applying and being accepted for a credit building loan. Those improvements continued over time — improving with an 11 point increase over 6 months, and 26-28 points at the 12-month mark.

Of course, to really understand why these strategies work, it’s important to understand how your credit score is calculated.

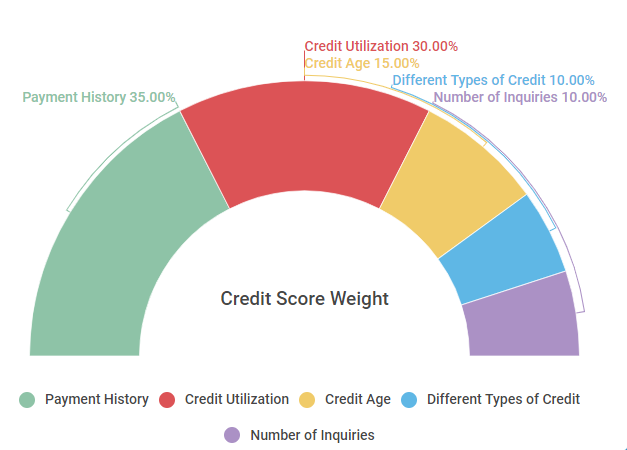

Factors in your credit score

Your FICO credit score is primarily made up of the following factors:

- Payment history. Your payment history has the single biggest impact on your credit score of all factors. Always make at least the minimum payment and make all your payments on time every month.

- Credit utilization. This is basically how much of your available credit you’re currently using. For the best score, you should aim to keep this number at or below 30 percent (some experts even suggest trying to stay below 10 percent, although this can sometimes be difficult).

- Length of credit history. The length of your credit history also factors into your score. Always keep your oldest accounts open and in good standing.

- Types of current credit. Creditors and lenders like to see responsible use of a mix of credit types. If you only have credit cards, consider adding a credit building loan. Similarly, if you only have something like a student loan on your credit report, consider applying for a credit card or store account card.

- Account inquiries. The number of credit inquiries for your account can also impact your score. Soft inquiries (when you check your credit yourself) do not affect your score, but a hard inquiry, such as when you apply for a new credit card, can. Limit the number of your applications for the best score.

This gives a broad overview of what your credit score is comprised of. Each factor is weighted differently depending on how important the credit agency believes it to be. So how does each factor affect your credit score?

FICO scoring model calculation (weight) factors

| Credit Factors | Credit Score Weight |

|---|---|

| Payment History | 35% |

| Credit Utilization | 30% |

| Credit Age | 15% |

| Different Types of Credit | 10% |

| Number of Inquiries | 10% |

Source: https://www.myfico.com/credit-education/whats-in-your-credit-score

Payment history and credit utilization are the two factors that most impact your credit score, with the age of your credit history coming in third at 15 percent. Now you know how your score is created, let’s look at what you can expect with a 610 credit score.

What can you expect with a 610 credit score

The interest rates you pay on various types of loans or lines of credit tend to be a direct reflection of your credit score. With this in mind, let’s take a quick look at the average interest rates for consumers with fair credit.

Interest Rate Ranges for Different Credit Score Ranks

| Type of Loan | Poor Credit | Fair Credit | Good Credit | Very Good Credit | Exceptional Credit |

|---|---|---|---|---|---|

| 30 Year Fixed Mortgage Interest Rate | 6.352% | 5.588% | 5.158% | 4.767% | 4.545% |

| Car Loan Interest Rate | 15.24% | 14.06% | 7.02% | 4.95% | 3.60% |

| Credit Card Interest Rate | 24.9% | 17.6% | 14.9% | 12.2% | 13.9% |

Source: Credit Sesame asked 400 members about their interest rates during a three week period beginning on January 18, 2018.

Someone with a 610 credit score, which falls into the fair credit range, pays significantly more in interest than someone with good or excellent credit. While these numbers may not seem greatly different, even a slight difference in the interest rate can have a huge financial impact when you consider the 30-year life of a mortgage or a 6+ year term of a car loan.

Can you get a car with a 610 credit score?

If you have a 610 credit score and are considering the purchase of a car, your credit score can, and will, affect not only your ability to get approved for a loan but also what percent interest you will pay. To help, we surveyed 600 Credit Sesame members with various credit scores to see how car loans were distributed in 2017.

Percentage of New & Used Car Loans Distributed Among Credit Rank of Consumers

| Credit Score | New Car Loan in 2017 | Used Car Loan in 2017 |

|---|---|---|

| Excellent (800+) | 24% | 16% |

| Very Good (750+) | 22% | 25% |

| Good (700+) | 19% | 28% |

| Fair (581+) | 17% | 18% |

| Poor (<580) | 13% | 13% |

Source: Credit Sesame followed 600 Members in 2017 documenting their choices for automobile financing and purchasing decisions and were divided by FICO Credit Score Ranking. The poll was conducted from January 2017 until December of 2017.

Only 17 percent of new car loans in 2017 went to consumers with credit scores in the fair range. Similarly, only 18 percent of used car loans went to the same group. If you’re trying to improve your chances of getting a car loan, you may also consider getting a cosigner for your loan, which will help improve your creditworthiness.

Can you get a credit card with a 610 credit score?

Can you get a credit card with a 610 credit score? The answer is yes, but keep in mind your interest rate will likely be higher than those with better credit.

Percentage of Credit Sesame Members Who Open New Credit Accounts in 2017

| Credit Ranking | Credit Cards | Store Credit Cards | Auto Loans | Mortgage Loans |

|---|---|---|---|---|

| Poor (<649) | 24% | 29% | 10% | 3% |

| Fair (<699) | 28% | 26% | 20% | 16% |

| Good (<749) | 22% | 20% | 25% | 19% |

| Very Good (<750) | 19% | 14% | 22% | 24% |

| Excellent (>800) | 15% | 7% | 33% | 25% |

Source: Review of 1000 Credit Sesame Members during December 2017 until December 2018. 167 participants made up each credit ranking (Bad, Poor, Fair, Good, Very Good, Excellent).

28 percent of consumers in the fair credit range were able to secure a credit card, with 26 percent opening store cards. If you’ve applied for a credit card and have been denied, consider asking a friend or family member with good credit to add you as an authorized user on their account. This can help improve your score drastically, at which point you can try again.

Dealing with negative information on your credit report

While there are processes in place for you to dispute inaccurate findings on your credit report, if the negative information on your report is accurate, it’s a waiting game for it to come off. But how long do negative marks stay on your credit report? Here’s a quick guide:

- Late payments or past due accounts: 7 years

- Collections: 7 years from original date of delinquency

- Hard inquiries: 2 years

- Bankruptcy: 7 years for Chapter 13, 10 years for Chapter 7

While negative elements stay on your credit report for some time, they have an immediate and negative impact on your credit score. Here is how negative marks can impact a 610 score:

Negative Impacts on Fair Credit Ranking over 6, 12, and 24 Months

| Negative Factor | 6 Months | 12 Months | 24 Months |

|---|---|---|---|

| Account Charged Off | -81 | -174 | -202 |

| Credit Collections | -48 | -70 | -123 |

| Loan Defaulting | -34 | -75 | -98 |

| Filing Bankruptcy | -88 | -121 | -162 |

| Home Foreclosure | -78 | -185 | -211 |

| High Credit Utilization | -16 | -29 | -43 |

| Closing Credit Card | -11 | -15 | -24 |

Source: Credit Surveyed 80 people with a Fair Credit Ranking who reported negative impacts to their credit score over a period of two years between February of 2015 and March of 2017. The numbers represent the average credit score points gained or lost by the stated factors.

As this graph shows, negative marks can have a huge impact on your credit score. This is why it’s important to do all that you can to keep your score in top shape.

Credit Sesame conducted a survey regarding credit report errors. Of those who responded, nearly 40 percent had at least one error on their credit report. It’s important to regularly check your report for any inaccurate or outdated information. If you find any errors, you have the right to dispute the mark and have it removed.

But what negative marks make the largest impact on your credit score?

Largest Impacts in Inaccurate Credit Reports

| Credit Ranking | Incorrect Information | Lender Closed Accounts | Old Debts | Duplicate Accounts |

|---|---|---|---|---|

| Poor | 33% | 34% | 18% | 15% |

| Fair | 29% | 32% | 31% | 8% |

| Good | 33% | 26% | 22% | 19% |

| Very Good | 1% | 3% | 1% | 6% |

| Excellent | 0.5% | 0% | 0% | 0% |

Source: Credit Sesame surveyed 250 people, 50 had a poor credit ranking, 50 participants had a fair credit score, 50 members had a good credit rating, 50 people were listed as very good, and 50 members reported they had an excellent credit score. The study was conducted on October 20, 2017, over a period of two weeks.

Among those with fair credit scores, the largest impact was caused by lender closed accounts, followed closely by old debt.

Credit Sesame member Roselee fixed her credit using our guidance.

Roselee Fixed her Credit Using These Steps

Member Since: 3/4/2017

| We interviewed Roselee on August 28, 2018; She is 48 years old, a single mother of one teenage son, and works as a secretary for a rental company. She lives in Daytona Beach, Fla. | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Were | you | able | to | fix | your | credit | score? | |||

| I didn’t think I would be able to at first, but I started slowly and I was able to fix it. Looking back, it was no one’s fault but my own, so I am glad that I learned more about credit scores and how important they are to one’s financial life. | ||||||||||

| What | was | your | original | score | and | what | is | your | score | now? |

| My original score was just fair. I never knew I was supposed to keep track of that type of stuff. The first time I checked it, it was 610. My score as we speak is 772, so I went up from fair to very good. | ||||||||||

| What steps did you take to improve your score, and how long did it take? | ||||||||||

| The first thing I did was look for any inaccuracies on my credit report, which I found that there were 6 of them. I sent letters regarding these to all three credit reporting bureaus and it took about 6 months for them to be cleared off. At the same time, I started to make sure that all my payments were made on time, and worked to get my credit cards under 30 percent. It took 16 months but I am finally closer to my personal goal of having excellent credit. |

The first thing that Roselee did was check for inaccuracies, and it should also be a priority for anyone looking to improve their credit.

TLDR; what can you do with a 610 credit score?

In conclusion, a 610 credit score is not the worst possible score you could have, but it definitely leaves room for you to grow. With a few smart strategies and some work on your part, it’s possible for you to boost your score using the methods we’ve discussed. For more ways to improve your credit score, check out this article.