You need a history of credit use to establish a credit score. Unfortunately, most lenders check your score before opening a line of credit. This means it can be a challenge to get started. Fortunately, there are ways around this that allow you to establish a credit score for the first time.

• Get a credit card—For your first credit card, try applying for a secured cards student card or retail credit card.

• Become an authorized user—Ask a trusted friend or family member with a great credit history to add you as an authorized user on one of their credit cards. Remember, this puts your credit health in their hands.

• Use Credit Sesame—We offer simple credit building solutions like Sesame Cash and Credit Builder, which use your debit purchases to establish and build your credit score.

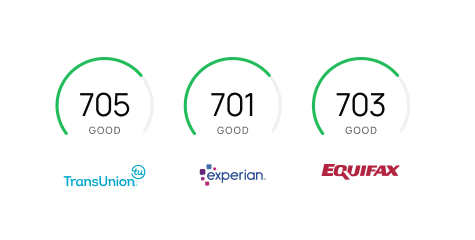

As soon as you start using credit, payments are recorded by the three major credit bureaus, TransUnion, Equifax and Experian. This establishes your credit history and your credit score.