If you’re just starting to establish your credit profile or credit history, you’re probably curious about what your starting score is. We’re going to look at what that score is, how it’s calculated, how you can improve it, and more.

What credit score do you start with?

You might be surprised to learn we all start out with no credit score at all. Your basic information isn’t reported until you’ve actually had credit (such as a credit card, loan, etc.) in your name for at least 6 months. However, this doesn’t mean that your credit score starts out at 0. There are 3 bureaus and each has their own unique scoring range, most of which start around 300.

Let’s take a closer look at credit score ranges, and how each bureau views them.

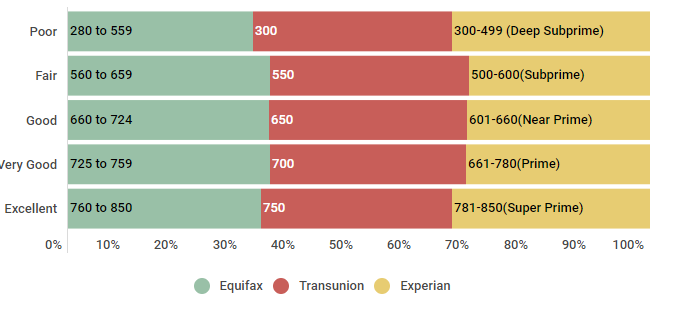

Credit Score Ranges: TransUnion (VantageScore 3.0), Equifax, Experian

| Rank | Equifax | Transunion | Experian |

|---|---|---|---|

| Poor | 280 to 559 | 300-550 | 300-499 (Deep Subprime) |

| Fair | 560 to 659 | 550-649 | 500-600(Subprime) |

| Good | 660 to 724 | 650-699 | 601-660(Near Prime) |

| Very Good | 725 to 759 | 700-749 | 661-780(Prime) |

| Excellent | 760 to 850 | 750-850 | 781-850(Super Prime) |

Source: Data found October 3, 2018. Experian Information Systems website. Credit Score FAQs. Retrieved from https://www.experian.com/blogs/ask-experian/credit-education/faqs/credit-score-faqs, Equifax website. Equifax Credit Score Range ™ US Only. Retrieved from https://help.equifax.com/s/article/Equifax-Credit-Score-ranges-US-only, TransUnion VantageScore 3.0 model.

As you can see, while each bureau has their own specific values that coordinate with the various credit score ranges, they are all relatively close in value. So, if your credit score doesn’t start at 0… where does it start?

What is your starting credit score?

We all start out with no credit score — which makes sense, given that our credit scores are based on the information contained in our credit reports, and these reports aren’t even generated until we have had credit in our names for 6 months or longer. Without an established history, your credit report and credit score don’t magically appear when you turn 18, despite many common misconceptions.

Once you have established credit, your first credit score could range anywhere from lower than 500 to well in the 700s, depending on your initial financial performance. The only connection between your first credit score and the scoring metrics would be the age of your credit profile. And given that this factor is only worth about 15% of the points in your total credit score, even by essentially ‘failing” this category and doing well in the others, you would still have a credit score well above 640.

Wondering what the credit scores of US consumers look like? Let’s take a closer look.

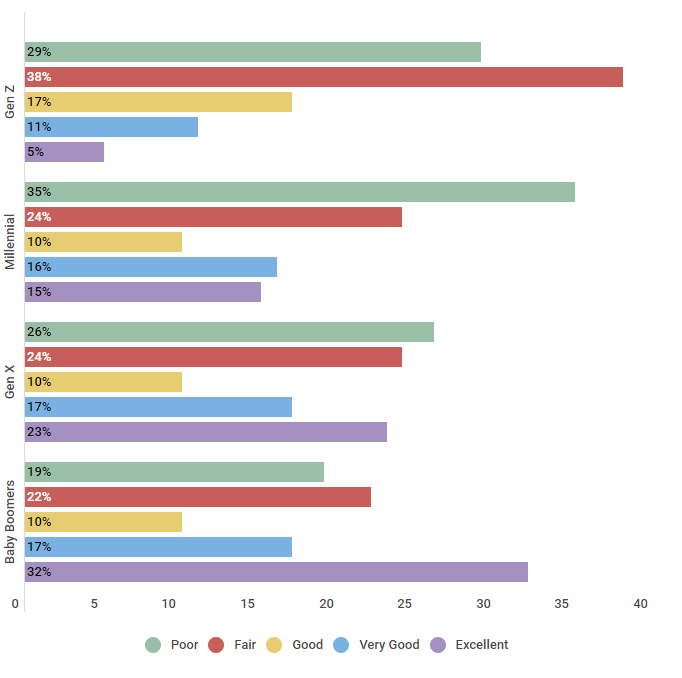

U.S. Population Categorized by the Five FICO Ranges for Credit Scores

| Age | Poor | Fair | Good | Very Good | Excellent |

|---|---|---|---|---|---|

| Gen Z | 29% | 38% | 17% | 11% | 5% |

| Millennial | 35% | 24% | 10% | 16% | 15% |

| Gen X | 26% | 24% | 10% | 17% | 23% |

| Baby Boomers | 19% | 22% | 10% | 17% | 32% |

Source: We ran a survey of 550 US consumers in different age groups on 9/26/2018 to understand which credit score ranges they fell into.

It comes as no surprise that older consumers with a more established credit history, have better credit scores — with approximately one-third of Baby Boomers having excellent credit. Younger generations that are just starting out in building their credit are still working on improving their scores, with the bulk of Gen Zers and Millennials having poor or fair credit.

Now that you know what scores look like, let’s see how they’re calculated.

How is your credit score calculated?

In order to understand how your credit score works, you have to know how it’s calculated. Your credit score has a number of factors that contribute to your score, each with its own weight. For the purpose of this article, we’re going to look at the factors that contribute to your FICO Score, since it is the most commonly recognized and used scoring method.

The factors that contribute to your credit score are as follows:

- Payment History (35%). Your payment history is the single biggest factor that contributes to your credit score. This shows potential lenders how often your payment have been on time — or if they have been late or missed.

- Credit Utilization (30%). While this may sound complicated, your credit utilization is simply the percentage of your total available credit that you are currently using. This number is expressed as a percentage and, to keep the best score, you’ll want to keep your number below 30%.

- Credit Age (15%). The age or length of your credit history also contributes to your score. To make the most of this factor, make sure to keep your oldest accounts open and in good standing.

- Credit Mix (10%). Potential lenders like to see a mix of different credit types on your report, such as credit card accounts and an auto or mortgage loan.

- Number of Inquiries (10%). While checking your credit score won’t hurt your account, hard inquiries, such as when you apply for a new credit card, will. Limit the number of hard inquiries on your credit to keep your score high.

Now that you know that your credit score is based on the information contained in your credit report, as well as how your credit score is calculated, let’s take a closer look at how you can check your credit report.

How to check your credit report

By law, you are entitled to one free copy of your credit report every 12 months, from each of the 3 nationwide credit reporting bureaus (Equifax, Experian, and TransUnion). You can request a copy of your credit report online from annualcreditreport.com (the only authorized website for these free credit reports) or by calling 1-877-322-8228. You will need to provide your name, address, social security number, and your date of birth in order to verify your identity.

But what if you’re told you have an insufficient credit history when you apply for credit or try to check your credit report?

What is insufficient credit history?

It’s not uncommon to have an insufficient credit history when you’re just starting out. Having an insufficient credit history simply means that your credit profile isn’t old enough to satisfy the requirements of a certain lender. If you’re told that you have an insufficient credit history, there are several strategies that you can take to help overcome this:

- Apply for a secured credit card

- Apply for a credit builder loan

- Ask your landlord to report your monthly rent payments

- Add an authorized user to your credit card, or become an authorized user on someone else’s account

If you have an insufficient credit history, it’s important to know that you’re not alone. Let’s take a look at the number of people who are currently credit invisible:

Americans who are credit invisible

| Generation | Percentage Who are Credit Invisible |

|---|---|

| Generation Z | 84% |

| Millennials | 24% |

| Generation X | 15% |

| Baby Boomers | 10% |

| The Silent Generation | 15% |

Source: Information obtained from the Consumer Financial Protection Bureau on October 11, 2018.

https://www.consumerfinance.gov/about-us/blog/who-are-credit-invisible/

As you can see, an overwhelming majority of Gen Zers (84%) are considered credit invisible. This number continues to drop as the generations get older. For instance, only 24% of Millennials are considered credit invisible, and a mere 10% of Baby Boomers are.

To learn more about insufficient credit history and the steps you can take to help build your credit profile quickly, check out these articles.

How long will it take to improve your credit?

If your starting credit score isn’t where you’d like it to be, you’re probably wondering how long it will take to see an improvement in your credit score. Let’s take a look below:

The Length of Time to Improve Credit Score and Move Into Different Credit Ranking

| Credit Score Range (Start) | Credit Score Range (End) | Average Time Taken |

|---|---|---|

| Poor Credit Score | Fair Credit Score | 8 Months |

| Fair Credit Score | Good Credit Score | 14 Months |

| Good Credit Score | Excellent Credit Score | 7 Months |

Source: We surveyed 455 consumers over the course of 24 months to understand on average how long it takes to move between credit ranges starting 2/15/2016 to 2/15/2018.

You can expect to see significant improvements fairly quickly. For instance, when actively working to improve your credit, you can expect to see your score improve from poor to fair in just 8 months.

| Related to "Starting Credit Score" |

|---|

| Free Credit Score |

| How To Build Credit |

| FICO Score |

| What is a Great Credit Score |

| Us Average Credit Score |

| FICO Score Definition |

What to expect with a starting credit score

If you’re just starting out with credit and your score falls in the “new” range, what can you expect if and when you need to make a major purchase? Unfortunately, your initial interest rates may be a bit higher than you’d like. If this is the case, consider adding a co-signer to your application, if that is a possibility. If it’s not possible to secure a co-signer, keep in mind that you can always refinance your purchase later on, once your credit score has improved.

Now, let’s look at the average interest rates Credit Sesame members are paying, based on their credit score range.

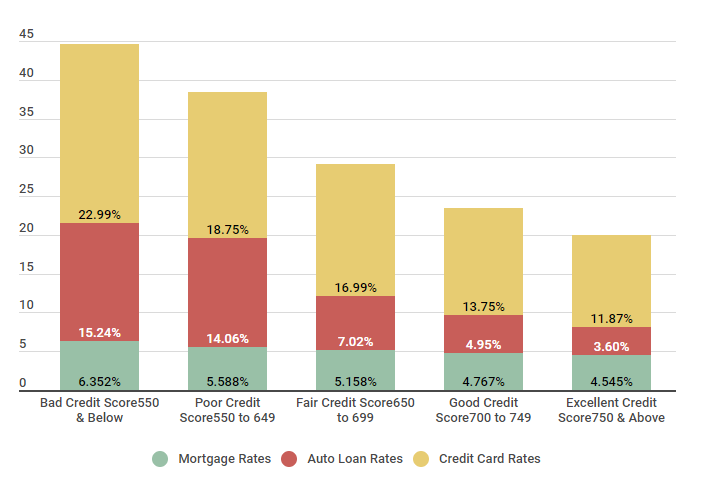

Comparing Average Interest Rates of Credit Sesame Members

| Score Range | Mortgage Rates | Auto Loan Rates | Credit Card Rates |

|---|---|---|---|

| Bad Credit Score 550 & Below | 6.352% | 15.24% | 22.99% |

| Poor Credit Score 550 to 649 | 5.588% | 14.06% | 18.75% |

| Fair Credit Score 650 to 699 | 5.158% | 7.02% | 16.99% |

| Good Credit Score 700 to 749 | 4.767% | 4.95% | 13.75% |

| Excellent Credit Score 750 & Above | 4.545% | 3.60% | 11.87% |

Source: Credit scores were calculated from 5,000 Credit Sesame members on 3/11/18.

As you can see, consumers with bad credit, unfortunately, end up paying significantly more in interest than those who have excellent credit. Take, for instance, credit card interest rates — if you have bad credit, you can expect to pay approximately 23% interest. With excellent credit, this number drops to less than 12% — meaning that if you have bad credit, you’ll end up paying nearly twice as much in interest charges, for the very same purchases.

We spoke to Credit Sesame member, Keilani, to find how what she’s doing to build her credit at 18 years old. Here’s what she had to say:

Keilani at 18 is already building her credit

Member Since: 9/1/2018

| We interviewed Keilani on September 25, 2018; she is 18 and lives in Honolulu, Hawaii. She works part-time at the international marketplace before college starts and makes 10.10 an hour. | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| We noticed you just joined, what prompted you to build your credit? | ||||||||||||

| I took a business class in high school when I was 16 and learned about the importance of credit scores and how they can influence your entire financial life. I did not want to depend on someone else for loans or credit cards so I set a goal to have a good credit score by the time I graduated. I heard from a customer about Credit Sesame and so I decided to check it out. I am so happy I did. | ||||||||||||

| What | is | your | credit | score | and | how | have | you | been | building | your | credit? |

| My credit score right now is 752, which is very good but not where I want it to be. I would like it to be excellent, but I understand with my limited credit history that would be difficult. After my class, I talked to my parents about adding me as an authorized signer on their credit card, which they did, somewhat reluctantly. They had every right to be worried, not all teenagers are responsible with money. Last summer I began working and at the beginning of my senior year, I asked my parents to co-sign on a very small loan for a car. Because of the money I saved up, I was able to make payments every month, and now it is almost paid off. | ||||||||||||

| So | what | do | you | plan | to | do | to | continue | building | your | credit? | |

| I plan on living at home during at least the first year of college, so I am going to save money that way. I am also going to apply for my own credit card. Because college is expensive I had to take out a student loan, which with my other loans help to diversify, and will continue to build my credit. I know it won’t be easy, but my goal is to have excellent credit before I graduate college so I can do anything I want. |

We wanted to share Keilani’s story because it shows the importance of building your credit from an early age, and how this can set you up for financial success in the future.

Conclusion & Summary

In conclusion, when you start out building your credit, your initial credit score doesn’t start out at 0. Each bureau has its own method for calculating your credit score, although they all revolve around similar factors. By making responsible choices with your credit, you’re well on your way to a good credit score — and all of the benefits that come along with it.