Credit Sesame on how it is possible to be cash rich and credit poor.

Money doesn’t solve everything. For some people, it isn’t even enough to keep them out of financial trouble.

A recent survey by Credit Sesame found that many people with above-average incomes have below-average credit scores, so-called cash rich and credit poor. That should be a warning sign for those people, and also a cautionary tale for everyone else.

This article will explore how people can be cash rich and credit poor. It will discuss why that can be a problem, and what consumers can do about it.

What does it mean to be cash rich and credit poor?

To understand how someone can be cash rich and credit poor, it helps to start by making distinctions between income, wealth and credit status:

- Income is the amount of money you have coming in every year. This can come from wages or investment earnings.

- Wealth is the amount of money you’ve accumulated so far. Whether it’s from savings, investment gains or equity in a home, wealth represents the cushion of resources you have to fall back on.

- Credit status is how potential lenders and others look at your reliability when it comes to handling debt. This is based on how you’ve used debt in the past and your current debt load.

To be cash rich means you either have a high income or have accumulated a good amount of wealth – or both.

However, that doesn’t necessarily mean you’d be considered a good credit risk. That’s based on your credit history, which is summed up by your credit score.

What determines your credit score?

Credit scores are based on the following five factors:

- Payment history. This measures how you’ve used credit in the past. If you’ve consistently and recently made all your debt payments in full and on time, it should help your credit score.

- Amounts owed. This is based not just on the dollar amount owed, but also what percentage of your available credit is in use. If you’re using a high portion of your credit limits, it can be a sign that you’re overextended and this hurts your credit score.

- Length of credit history. The longer you’ve had credit accounts and the more history you have of using them, the better established you credit record is.

- Credit mix. The borrowing and payment terms vary for different types of credit. For example, using a credit card (revolving credit) is very different from having a mortgage Installment credit). Having a mix of both revolving credit and installment loans can help your credit score.

- New credit. If you’ve recently opened several new credit accounts it can increase the risk that you’ll get in over your head. That can drag down your credit score.

None of these factors involves how much money you make or how much wealth you have. That’s why having a lot of cash doesn’t necessarily go hand-in-hand with good credit.

Do some people with high incomes have bad credit?

How likely is it that someone with a high income would have bad credit?

The Credit Sesame survey compared incomes with credit scores. As you might expect, it found that people with above-average incomes generally have above-average credit scores.

However, the survey also found that this isn’t always the case. Though they were in the minority, a significant portion of above-average earners reported having below-average credit scores.

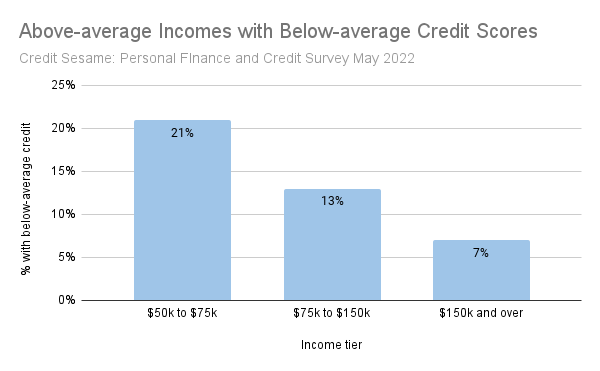

According to the Bureau of Labor Statistics, the median income in the United States is $45,760. As shown by the graph below, even some portion of Americans earning above that amount had below-average credit scores:

Just over one out of five people making between $50,000 and $75,000 reported having below-average credit scores. Among people earning from $75,000 to $150,000, about one in eight had below-average credit.

As you can see by the third income category, even among people making $150,000 or above there were cases of people with below-average credit scores.

How do high earners get bad credit?

So how does this happen? How can you be making good money and still end up with bad credit?

Here are three ways that can happen:

- Not using credit. If you haven’t used credit at all or haven’t used it recently, you may not have enough history to have earned a good credit score. You may have a poor credit score, or even be considered credit invisible — someone who has no credit record.

- Living beyond one’s means. For some people, even a good income is not enough to support the lifestyle they want. So they supplement their income with borrowing. This can’t go on forever though, so eventually they find themselves with bills they can’t pay — and bad credit.

- Being careless with credit. Using credit responsibly isn’t just a matter of having the money to pay what you owe. You also have to be organized and conscientious enough to make your payments on time. If you don’t keep up with that obligation, no amount of money will save you from having a poor credit score.

Why even high earners need good credit

You might wonder why high earners should they care about their credit scores.

Well, even high earners might not be able to pay for a new car out of their normal cash flow, let alone for a house. In that case, they’d have to apply for a loan.

Also, beyond big-ticket items, the convenience of using a credit card is important. That’s especially true if you travel frequently.

Finally, aside from borrowing, credit scores are often used by employers, landlords and insurance companies to evaluate people. A poor credit score can restrict your opportunities and cost you money.

Tips for improving credit

Here are some of the basic ways you can improve your credit score:

- Use credit moderately and consistently. Don’t shy away from using credit. A good credit score comes from proving over time that you can borrow money and pay it back.

- Limit your credit balances. Don’t carry big balances on your credit cards. Not only is this expensive, but using a high portion of your available credit hurts your credit score.

- Organize your payments. Work out a system to make sure you keep up with your payments. If you use autopay, make sure there is enough money in your bank account to cover the bills when they come due.

- Pick your spots when opening and closing accounts. Too many new accounts can hurt your credit score. But, since older accounts can be a positive, don’t be too quick to close accounts.

Certainly, if you have a high income it should make it easier to develop a good credit score. But it’s no guarantee. You have to work on it or you will remain cash rich and credit poor.

You may also be interested in:

Disclaimer: The article and information provided here is for informational purposes only and is not intended as a substitute for professional advice.

Survey methodology

The Credit Sesame Personal Finance and Credit Survey May 2022 was designed and executed by Credit Sesame using the Momentive Inc. survey tool. General population data was collected online May 20-21, 2022. The survey sample comprised 1,222 U.S. residents aged 18 to 99 years balanced for age and gender using U.S. Census data. The sample data is accurate to within +/- 2.888 percentage points using a 95% confidence level.