According to Credit Sesame’s Personal Finance and Credit Survey May 2022, it is possible to have a low income and a high credit score.

There is an expectation that low income earners have low credit scores. In fact, the data show low earners can beat the odds and earn good credit scores. High income earners may have an easier time maintaining a good credit score, but it is no guarantee. Some people with high salaries have low credit scores despite the income at their disposal. And some low earners have high credit scores.

When it comes to having a good credit score, it isn’t how much you earn that matters. It’s how you manage your money and debt.

This article explains how to join the successful consumers who’ve beaten the odds by achieving good credit scores despite low incomes.

Low income and a high credit score in America

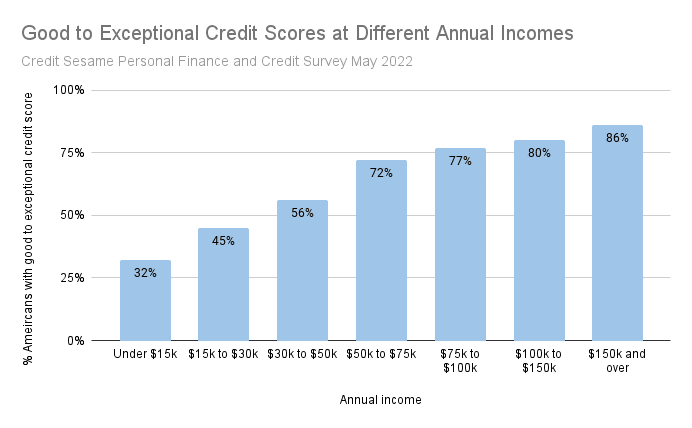

As you might expect, there is a correlation between income and credit score. High earners are generally more likely to have strong credit histories than low earners. The chart below shows that the percentage of consumers with good-to-exceptional credit scores rises with each step up in income level.

However, this same chart also shows that not everybody with relatively low incomes is doomed to having bad credit. For example, people in the $30,000 to $50,000 range earn less than the average annual wage of $58,260, according to the Bureau of Labor Statistics. And yet, the chart shows that more than half of these below-average earners have good-to-exceptional credit scores.

Perhaps more remarkably, among people earning less that $15,000 a year nearly a third (32%) managed to have good-to-exceptional credit.

On the flip side, among people earning from $100,000 to $150,000, 12% have very poor to fair credit.

So, a strong income is no guarantee of good credit. On the plus side, a low income does not mean you have to settle for poor credit. A low income and a high credit score is possible.

Why good credit is especially important with low income

Not only can you have good credit on a low income, but it’s especially important for people with limited budgets.

Here’s why people with low incomes might benefit most from having a strong credit history:

- The need for financial flexibility. Access to credit gives you more flexibility as to where you shop and when you buy. Being able to look for bargains online and make a purchase when you see a good deal can save you money. It’s harder to do these things if you rely on cash alone.

- Minimizing interest costs. The better your credit, the lower the interest rates you’re likely to be charged. On a limited budget, every dollar you save makes a difference.

- Potential to build wealth through home ownership. On a low income, being able to get a mortgage is potentially your only realistic means of buying a home. This is one of those things that widens the gap between haves and have-nots. Home owners generally build wealth over time as property values rise. On the other hand, renters see their wealth eroded more and more as rents increase.

Low income and high credit score tips

The numbers show that it is possible to have low income and a high credit score. So, how is this done? Actually, there are several pathways to a good credit score even if your income is low. Here are some examples:

- Student loan payments are a good way to start building credit. One of the challenges people have in building a credit history is being able to get credit in the first place. However, federal student loans are widely available, so people who have them should look at making payments on them as a chance to show they can use credit responsibly.

- Secured loans can create a pathway to credit. Loans that are backed by collateral are often easier to get than unsecured loans. Car loans are a good example. If you are sure you can afford the payments, a car loan can be a good way to start establishing a credit history.

- Secured credit cards are another option. As with secured loans, secured credit cards are often easier to get than unsecured ones. It requires that you provide a deposit, but that might be worthwhile if it’s a way to build a payment history. Do that successfully, and you should soon graduate to being able to qualify for a conventional credit card.

- Shop around for the best terms. The Federal Reserve’s 2019 Survey of Consumer Finances found that high earners tend to shop for credit terms more intensely than low earners. That’s unfortunate, because more favorable interest rates and other terms increase your chances of using credit successfully.

- Use credit as a cash alternative. The best way to use credit is as a cash alternative. You charge a purchase to a credit card rather than paying with cash, but pay off the balance in full by the next due date. Doing that lets you avoid interest charges while building a steady payment history.

- Keep up with every payment. Think of starting to use credit as an audition. Once you get that opportunity, you have to make the most of it. That means using it to prove you can be relied on to make all your payments on time and in full.

Credit traps low-income consumers should avoid

In contrast to the credit-building habits described above, too often low-income consumers fall into credit traps that damage their finances:

- Assuming they can’t get credit. It’s harder to get access to credit with a low income, but as discussed in the previous section it can be done. Don’t assume there isn’t a way in.

- Using payday lenders. Instead of establishing conventional credit, poorer Americans too often resort to payday lenders. The extravagant amount these lenders charge for short-term loans helps make the poor poorer.

- Borrowing long-term for short-term expenses. Once you get credit, use it wisely. First of all, you should only use a credit card for the short-term. Credit cards are too expensive if you carry long-term balances on them. Also, you should not be borrowing long-term to meet routine expenses. That only causes you to fall further and further behind.

- Failure to prepare for emergencies. Not having some emergency savings to fall back on forces people to borrow when an unexpected setback happens. This only increases the cost of that emergency.

- Overpaying for credit. If you’re going to pay interest, you want to keep the rate low as possible. Unfortunately, between letting their credit scores slip and not shopping for better terms, poorer Americans too often pay more for credit than they have to.

Not everybody has the opportunity to earn a high income. However, you can make the most of what you’ve got by using credit wisely. The Credit Sesame survey found many low earners are able to do just that. Low income and a high credit score is achievable.

You may also be interested in:

- Ten Ways to Build Credit on a Budget

- How to Develop Good Habits for Building Credit Score

- The Challenges of Having No Credit or a Low Credit Score

Disclaimer: The article and information provided here is for informational purposes only and is not intended as a substitute for professional advice.

Survey methodology

The Credit Sesame Personal Finance and Credit Survey 2022 was designed and executed by Credit Sesame using the Momentive Inc. survey tool. General population data was collected online May 20-21, 2022. The survey sample comprised 1,222 U.S. residents aged 18 to 99 years balanced for age and gender using U.S. Census data. The sample data is accurate to within + 2.88 percentage points using a 95% confidence level.