If you’re looking to purchase a home, an FHA loan is often a great option. Let’s look at the loan qualifications, including the credit score you’ll need to qualify for an FHA loan.

What are the minimum credit score requirements for an FHA loan?

FHA loans can often bring home ownership into the hands of people who may otherwise have a hard time getting approved for a mortgage with traditional lenders. There are a number of benefits to FHA loans, including a lower down payment, approval with thin credit or problems with your credit profile, extra funding for renovations, and more.

In order to qualify for an FHA loan, you must have at least a 500 credit score — however, a credit score of 580 is the tipping point between having to make a 10% down payment and being able to make a smaller 3.5 percent down payment.

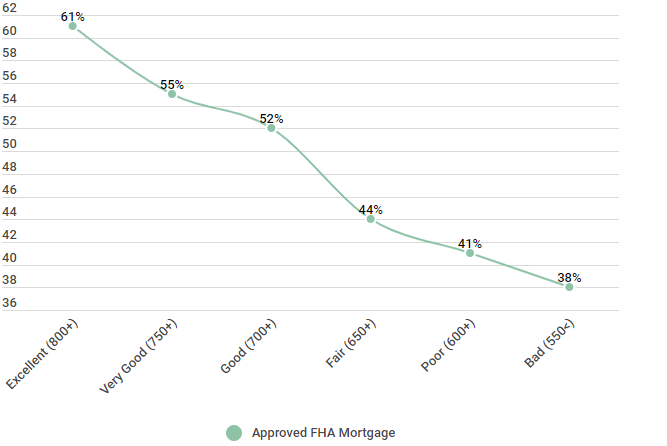

Let’s take a closer look at the number of FHA loan approvals by credit score range.

FHA loans approved by credit score range

| Credit Ranking | Approved FHA Mortgage |

|---|---|

| Excellent (800+) | 61% |

| Very Good (750+) | 55% |

| Good (700+) | 52% |

| Fair (650+) | 44% |

| Poor (600+) | 41% |

| Bad (550<) | 38% |

Source: The survey included 650 Homeowners with approved FHA mortgages. The study divided respondents by credit ranking. The poll was taken in June of 2018.

As you can see, there are a significant numbers of approvals, regardless of credit score ranking. Even among those consumers with a credit score lower than 550, the approval rating was nearly 40%.

Why is it important to know the credit requirements for an FHA loan?

If you’re trying to buy a home, knowing the different requirements for the most popular loan types can help you make educated decisions on which loan is the right one for you. Finding a mortgage loan that works for you will not only make it easier for you to be approved, it can also save you a significant amount of money in the process.

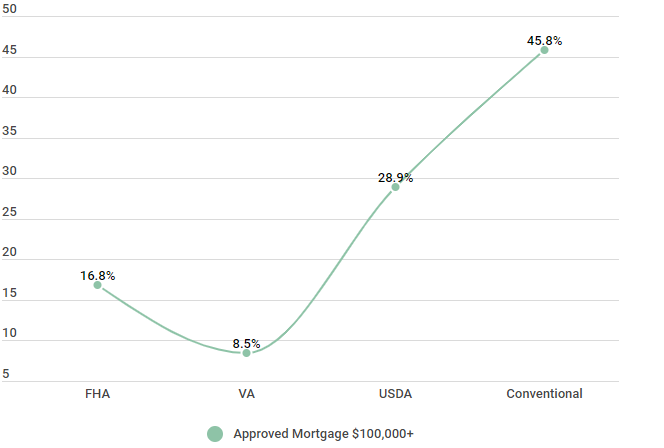

Now, let’s see what types of loans were being approved in 2017.

Mortgage type breakdown by loan, 2017

| Mortgage Loan Type | Approved Mortgage $100,000+ |

|---|---|

| FHA | 16.8% |

| VA | 8.5% |

| USDA | 28.9% |

| Conventional | 45.8% |

Source: The survey included 650 Homeowners with approved mortgages. The study divided respondents by credit ranking and asked them what type of loan they received. The poll was taken in June of 2018.

It’s easy to see that conventional mortgage loans and USDA mortgage loans are the big players in the game, representing nearly 75% of all mortgage loans approved in 2017. However, FHA loans were the third most approved type of loans, representing nearly 17% of all mortgage loans approved in 2017.

So what exactly is an FHA loan?

| Credit score |

|---|

| Good fico score |

| Average american credit score |

| Low credit score mortgage lenders |

| Mortgage interest rates based on credit score |

| First time home buyer no credit |

What is an FHA loan?

An FHA loan is a mortgage loan guaranteed by the FHA, or the US Federal Housing Administration. Private lenders, such as bank or credit unions, issue the loan and the FHA provides backing for it — in other words, if you don’t repay your loan, the FHA will step in and pay the lender instead. Thanks to this guarantee, lenders are more willing to make more substantial mortgage loan, and in cases where they would likely be otherwise unwilling to approve loan applications.

Founded in 1934 during the Great Depression, the Federal Housing Administration is a government agency that supplies mortgage insurance to private lenders. Before the introduction of the FHA, the US housing market was struggling. Less than 48% owned homes, and loans were not easy for buyers. For instance, borrowers were only able to finance approximately half of the purchase price of a home (as opposed to a small down payment), and then loans usually required a large balloon payment after a few years.

- There are a number of benefits to an FHA loan, including:

- Small down payment (as low as 3.5 percent)

- Easier to use gifts for down payment or closing costs

- Assumable loans

- A chance to reset poor credit

- Certain FHA loans can be used for home improvements

But how do you know if you qualify for an FHA loan?

What credit score do you need for an FHA loan?

You need to have at least a 500 credit score to qualify for an FHA loan. However, a credit score of 580 is the tipping point for being able to make a smaller 3.5 percent down payment, versus a 10% down payment.

When compared to traditional mortgages, FHA loans are easier to qualify for. Here are a few things to keep in mind if you’re considering an FHA loan.

- Check with various lenders. Of course, private lenders often set their own standards stricter than the minimum FHA requirements. If you’re having trouble qualifying with a particular lender, trying moving on to another. It never hurts to shop around when you’re looking for a mortgage.

- Income limits. While there is not specified minimum income necessary to qualify for an FHA loan, you do have to be able to prove that you are able to repay the loan. While there are no income limits for these loans, they are geared toward lower-income applicants. However, if you have a high income, you won’t be disqualified, as you may be with some other first time homebuyer programs.

- Debt to income ratios. To qualify for an FHA loan, you also need to have a reasonable debt to income ratio. In other words, the amount you spend on monthly loan payments should be relatively low, when compared to your income.

- Loan amount. The FHA also limits how much you are able to borrow. Generally speaking, you’ll be limited to a modest loan amount, relative to the home prices in your area. You can visit HUD’s website to find out your local maximum.

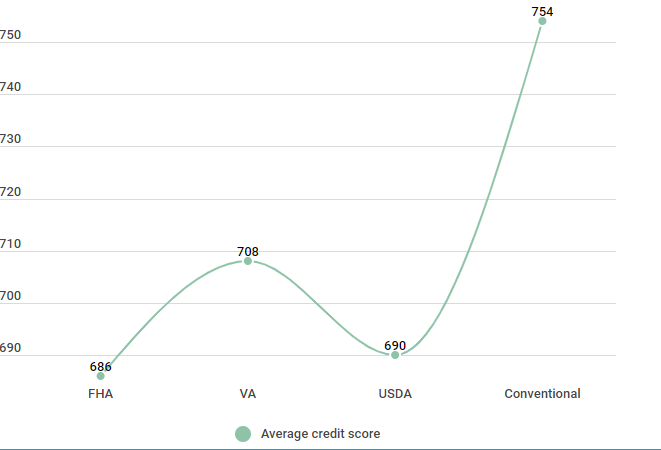

Let’s take a look at the average credit score for each type of mortgage loan.

Average credit score by mortgage type.

| Mortgage Loan Type | Average credit score |

|---|---|

| FHA | 686 |

| VA | 708 |

| USDA | 690 |

| Conventional | 754 |

Source: The survey included 650 Homeowners with approved mortgages. The study asked what their credit score was and what type of loan they received. The poll was taken in June of 2018.

As you can see, FHA loans are a great option for those with lower credit scores. Compared with a conventional mortgage loan, where borrowers have an average credit score of higher than 750, the average consumer with an FHA loan has a credit score of 686 — making this a much more attainable option for more consumers.

What are the FHA loan limits?

As mentioned above, you are limited in the amount that you can qualify for with an FHA mortgage. Let’s look more closely at the limits of a few different types of mortgage loans.

Loan limits by popular mortgage loan types for 2018

Description: A comparison of what the loan limits are for popular mortgage loan types for FY 2018

| Mortgage Loan Type | Loan Limit |

|---|---|

| FHA Forward - One family (Basic Standard) | $294,515 |

| FHA Forward - One family (High Cost Area) | $679,650 |

| VA (Most locations) | $453,100 |

| USDA | Varies by state, county, and town |

| Conventional | $453,100 |

Source: https://entp.hud.gov/idapp/html/hicost1.cfm, https://www.military.com/money/va-loans/home-purchase/va-loan-limits-for-high-cost-counties.html, https://www.fhfa.gov/Media/PublicAffairs/Pages/FHFA-Announces-Maximum-Conforming-Loan-Limits-for-2018.aspx, https://www.rd.usda.gov/files/RD-SFHAreaLoanLimitMap.pdf

Compared to VA Loans and conventional mortgage loans, you can see a marked difference in the FHA Forward loan. VA and conventional loans both allow for a loan limit of $453,100 — however, a basic standard FHA Forward loan allows for $294,515. This is another example of how FHA is geared towards low-income owners. The higher the loan, the higher the monthly mortgage payment will be, and so while the FHA could have a higher limit, it would not fit with their intended market.

Improving your credit score for an FHA loan

If your credit score isn’t where you want it to be, there are steps you can take to improve your score. There are several factors that contribute to your credit score, each with their own weight. Let’s take a closer look below:

- Payment History (35%). Your payment history is the single biggest factor that contributes to your credit score. This shows potential lenders how often your payment have been on time — or if they have been late or missed.

- Credit Utilization (30%). While this may sound complicated, your credit utilization is simply the percentage of your total available credit that you are currently using. This number is expressed as a percentage and, to keep the best score, you’ll want to keep your number below 30%.

- Credit Age (15%). The age or length of your credit history also contributes to your score. To make the most of this factor, make sure to keep your oldest accounts open and in good standing.

- Credit Mix (10%). Potential lenders like to see a mix of different credit types on your report, such as credit card accounts and an auto or mortgage loan.

- Number of Inquiries (10%). While checking your credit score won’t hurt your account, hard inquiries, such as when you apply for a new credit card, will. Limit the number of hard inquiries on your credit to keep your score high.

Benefits of learning about FHA loan requirements

There are benefits to learning about FHA loans, as well as the other types of mortgage loans that are available. A home is often the biggest financial purchase you will make, so it pays to do your due diligence. If you qualify for an FHA mortgage loan, and you are willing to work within their loan limit parameters, an FHA loan can be a great way to save a significant amount of money.

TLDR; what credit score do you need for an FHA loan?

To recap, an FHA loan is a type of mortgage loan that is insured by the Federal Housing Administration. If you fail to repay your loan, the FHA will repay your lender on your behalf — leading lenders to approve loans in cases where they otherwise may not. Additionally, FHA loans are designed for easier approval — with a minimum credit score requirement of 500.

Regardless of the type of mortgage loan you are applying for, it benefits you to get your credit in top shape before submitting your application. Follow these steps to improve your credit score in as little as 30 days, and you’ll be moving into your new home in no time.