If you’re one of the many Americans currently working to improve your credit, you probably want to know more about how often your credit report and score updates. Trying to improve your credit score can feel like a waiting game, but it actually doesn’t take long to see significant changes — if you’re using the right strategies.

How long does it take to see an improvement in your credit score?

When you’re trying to improve your credit score, time can seem to crawl as you’re waiting to see an updated score. You may be disheartened by how slowly changes to your score seem to happen, but even a month can make a significant difference to your score. What’s more, you may be surprised to find out how often credit scores are updated. In other words, you may be able to see progress sooner than you think.

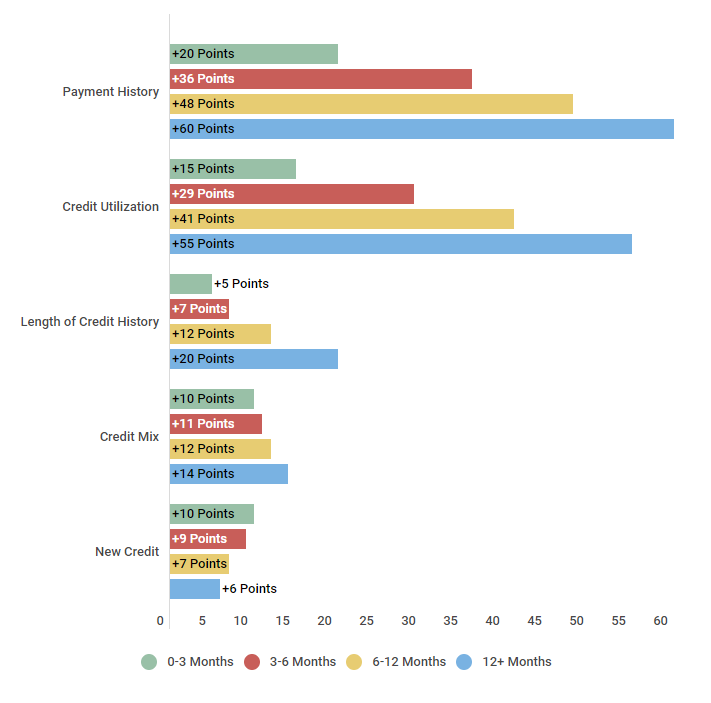

Let’s take a closer look at the average length of time of time it takes to see improvements to your credit score. When you’re working on improving your credit score, it’s easy to see from the data below that the biggest changes can be seen when focusing on your payment history and credit utilization (+60 points and +55 points, respectively, at 12 months). However, any improvement is good, so be sure to keep your oldest accounts open and don’t neglect the other factors.

Average length of time to see credit score improvement while proactively working on it

| Credit Score Factors | 0-3 Months | 3-6 Months | 6-12 Months | 12+ Months |

|---|---|---|---|---|

| Payment History | +20 Points | +36 Points | +48 Points | +60 Points |

| Credit Utilization | +15 Points | +29 Points | +41 Points | +55 Points |

| Length of Credit History | +5 Points | +7 Points | +12 Points | +20 Points |

| Credit Mix | +10 Points | +11 Points | +12 Points | +14 Points |

| New Credit | +10 Points | +9 Points | +7 Points | +6 Points |

Source: Survey of 750 members who actively worked on improving their credit score. Survey completed over the course of 24 months from 2/15/2016 – 2/15/2018.

What is a credit score?

Your credit score is a numerical score or representation of the information that can be found in your credit report, as reported by your lenders. Your credit report contains a detailed history of how you borrow and repay your debts. This information gets fed through a credit scoring model, such as FICO or VantageScore, and out comes your credit score.

Typically, lenders report information, both positive and negative, to the three credit bureaus (TransUnion, Equifax, and Experian) once a month. In other words, your credit score changes each month, depending on what new information is landing on your credit report and/or what old information is falling off.

What factors can change your credit score?

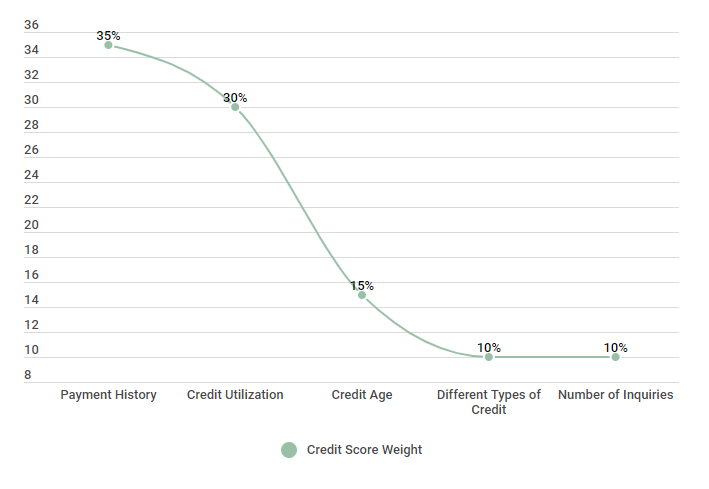

Now that you know that your score updates frequently, you might be wondering how it’s actually calculated — and what factors may cause a change to your score. Fortunately, it’s a pretty simple formula. For this article, we’ve chosen to focus on the FICO scoring model, since it is currently the most widely used scoring model (and has been for some time).

As you can see from the data below, your FICO score is calculated by looking at several factors:

- Payment history. This is simply a history of your payments — when you’ve paid on time, when you’ve paid late, when you’ve missed payments, etc. This is the single largest factor that contributes to your score, so it’s important to take it seriously. Always make your payments on time, every time.

- Credit utilization. Your credit utilization is simply the percentage of your combined credit limits that you are currently using. You should always strive to keep this number at or below 30%; however, those with the very best credit scores often keep their credit utilization below 10%.

- Credit age. The length of your credit history also plays a role in what your credit score will be. Lenders like to see a long history of responsible credit use, so the longer your oldest accounts have been open, the better off you’ll be. Always keep your oldest accounts open, even if you don’t use them on a regular basis.

- Different types of credit. Another factor in your score is the diversity in your credit. It will benefit your score to have various types of credit featured on your report, such as a car or mortgage loan and credit cards.

- Number of inquiries. The number of inquiries into your credit can also impact your score. Soft inquiries, such as when you check your own credit, won’t hurt your score — but hard inquiries, such as when you’re applying for a loan or a new credit card, will. Try to limit the number of applications for new credit to keep your credit score in the best shape. This does not mean don’t shop around for fear of multiple inquiries. If you are intending on buying a large item, such as a house or a vehicle, numerous credit inquiries within a short amount of time are counted as one inquiry versus multiple.

As you can see below, each of these factors have different weights — meaning that they impact your score to different degrees. For instance, your payment history contributes to 35% of your credit score, while the number of inquiries into your credit only contributes to 10%.

FICO Scoring Model Calculation (Weight) Factors

| Credit Factors | Credit Score Weight |

|---|---|

| Payment History | 35% |

| Credit Utilization | 30% |

| Credit Age | 15% |

| Different Types of Credit | 10% |

| Number of Inquiries | 10% |

Source: https://www.myfico.com/credit-education/whats-in-your-credit-score

Credit scores can fluctuate month to month

More often than not, changes to your credit score will occur in increments.Typically, you will only see changes of a few points each month — either up or down. Even though your credit score looks like it stays pretty consistent month to month, it can add up to big changes over time. However, there are a few instances when major changes to your credit score (25 points or more) can happen quickly, in just a month or two. Usually, these are a direct result of changes to either your payment history or your credit utilization, the two biggest contributing factors to your credit score (35% and 30%, respectively).

We spoke with Credit Sesame member, Zach to find out how he improved his credit over a 12 month period. Here’s his story.

Zach improved his credit over 12 months

Description: Zach has been a Credit Sesame member for 18 months, beginning right after his childhood best friend bought a house and they were discussing what the process was. Zach is 26 years old and realized during his conversation that he was nowhere near being ready for a house, or even a car, although he did have a good job working as a researcher for a large museum.

| Positive Factor | Update Date | Change | Score |

|---|---|---|---|

| Monthly Payments on time | August 2017 | +5 | 732 |

| Asked his landlord to report payments | September 2017 | +11 | 743 |

| Became an Authorized User on Grandmother’s Credit Card | December 2017 | +15 | 758 |

| Credit Request (Credit Card Application) | March 2018 | +10 | 768 |

Source: Zach submitted his story in September 2018.

Zach’s story is important because it shows the importance of the basics, such as making all of your monthly payments on time. Now, let’s take a closer look at how missing payments or delinquencies can affect your credit.

| Related To "Credit Score Updates" |

|---|

| Free Credit Score |

| What Is a Good Credit Score |

| How To Increase Your Credit Score |

| Building Credit |

| How To Fix Your Credit |

| Max Credit Score |

Delinquencies have a big impact on your credit

As shown in the data above, your payment history is the biggest single factor in your credit score. As such, making a significantly late payment (30 days or more) will almost always cause your score to take a big hit. But what if you’ve already fallen behind on one (or more) of your accounts? Do your best to get your account to a current status as quickly as you can — the older your delinquency, the more significant the damage to your score, so it pays to get back on track quickly.

Here’s some data on late payments and how they can hurt your credit score. As you can see, the longer your payment is late, the worse it is for your credit score. For instance, at 30 days late, you can expect a 25 point drop in your score. But once your payment reaches 60 days late, your score can drop nearly 50 points — and the trend continues from there.

Late Payment Delay & Credit Score Drop

| Late Payment (Days) | Average Credit Score Drop (TransUnion) | Average Credit Score Recovery (TransUnion) in 6 Months |

|---|---|---|

| 30 Days | 25 Points | 85 Points |

| 60 Days | 45 Points | 65 Points |

| 90 Days | 65 Points | 40 Points |

| 150 Days | 100 Points | 35 Points |

| Charge Off | 150 Points | 20 Points |

Source: We tracked a group of 500 members targeting those who have missed payments on their loans for different amounts of time and how much their credit score dropped during those time frames.

If your credit card company charges off your account, your credit score will take a massive 150 point hit, so it’s important to work with your lenders to keep your accounts current. And keep in mind that many lenders will even establish a payment plan that you can afford until you can get back on track.

The impact of debt load on your credit cards

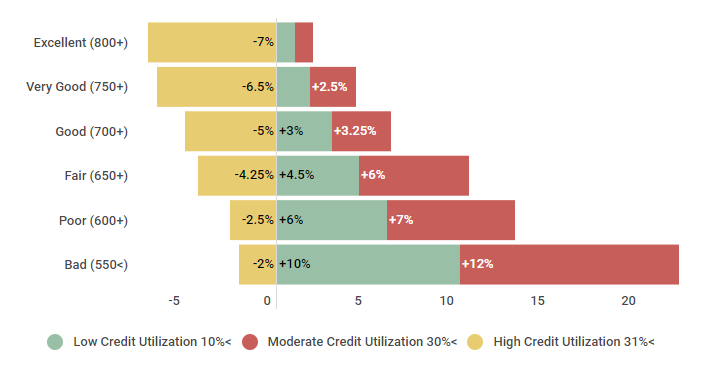

Another large factor of your credit score is your credit utilization, or the ratio of your used credit to total available credit. A spike in your credit card debt will cause your utilization to rise — and your score to likely drop. But keep in mind that the opposite effect is also true. Paying off some of your credit card debt will make your credit utilization more appealing to lenders, and can cause your scores to improve significantly in just one month.

What kind of changes to your credit score can you expect based on your credit utilization? Take a look at the table below.

Credit Score Improvements By Lowering Credit Utilization

| Credit Ranking | Low Credit Utilization 10%< | Moderate Credit Utilization 30%< | High Credit Utilization 31%< |

|---|---|---|---|

| Excellent (800+) | +1% | +1% | -7% |

| Very Good (750+) | +1.8% | +2.5% | -6.5% |

| Good (700+) | +3% | +3.25% | -5% |

| Fair (650+) | +4.5% | +6% | -4.25% |

| Poor (600+) | +6% | +7% | -2.5% |

| Bad (550<) | +10% | +12% | -2% |

Source: Credit Sesame surveyed 600 Americans on how credit utilization impacts their credit scores. Groups were divided by Credit Rank (Bad, Poor, Fair, Good, Very Good, and Excellent) and then subdivided by Low Credit Utilization, Moderate Credit Utilization, and High Credit Utilization. The study took place October 2015 until November of 2016.

For those with bad credit, this can make a big difference — by lowering their credit utilization to below 30%, these consumers can expect to see a 12% improvement in their score.

TLDR; how often is your credit score updated?

To recap, your credit score is a three-digit number that is a direct reflection of the information contained in your credit report. Your credit score is calculated by looking at 5 distinct factors (payment history, credit utilization, credit age, credit mix, and number of inquiries) and can fluctuate month to month. By utilizing smart credit strategies, you’ll be able to see changes to your credit score — maybe even faster than you think.