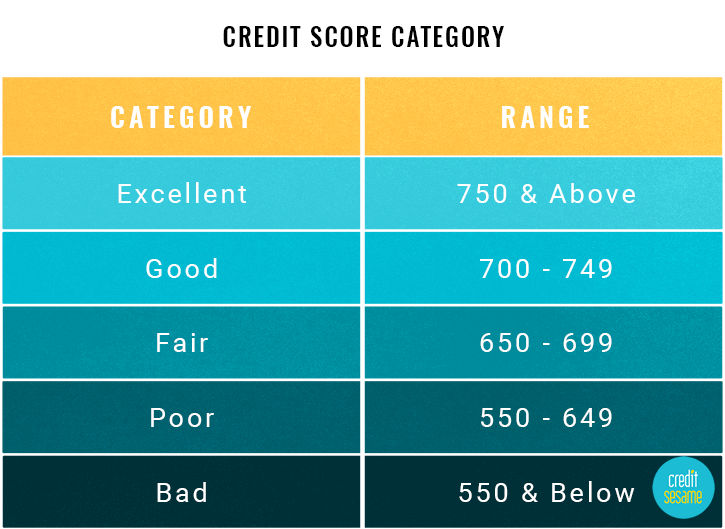

You may know that a FICO® score of 740 and above is generally considered excellent, while a score of 550 and below is poor.

What if your score is hovering near the cusp of two credit score ranges, where just a few points could bump you into the next category? In that case, a small handful of points could save you thousands of dollars in interest, depending on the type of credit you seek.

What are the credit score ranges?

The most widely used consumer credit scores are based on the FICO® or VantageScore® scoring models and calculated by any of the three major credit reporting agencies: TransUnion, Equifax, and Experian. The most current versions of FICO® and VantageScore® range from 300 to 850.

FICO® and VantageScore® don’t say whether a credit score is poor, excellent or anywhere in between. In fact, neither do the credit bureaus.

Each lender decides what constitutes a bad, poor, fair, good or excellent credit score, as well as exactly what range of credit scores falls into each category. Here’s an example:

FICO® and VantageScore® update their scoring systems every so often. The latest model from FICO® is the FICO® 9. The latest model from VantageScore® is the 3.0, and that’s the free credit score Credit Sesame offers.

What can cause your credit score to change a few points?

Average account age goes up. Your credit score gets better over time. Every month that passes, your average age goes up a little. The average account age is the age of all of your credit accounts divided by the number of accounts.

Even closed accounts factor into your average account age.

- Accounts closed in good standing remain on your credit report for ten years

- Accounts closed in default remain for seven years

- Open accounts remain indefinitely

Closing an account does not immediately affect your average account age, but will when enough time passes and the account is removed from your credit file.

Average account age goes down. We see average account age go down when we open new accounts.

If you’ve got a student loan that’s 10 years old and an auto loan that’s two years old, your average account age is six years. If you open a new credit card, your average account age drops to four years.

Your average account age might also suffer when a long standing account ages off your report. For example, perhaps you paid off your student loan ten years ago after making payments for 20 years. This year, you lose the benefit of those 30 years when the account ages off your credit report.

Open or close a credit card. The reason opening or closing a credit card can immediately affect your credit is because it affects your credit utilization, a huge part of your credit score. That’s the amount of revolving debt you owe in relation to your credit limits. It’s calculated for each card and overall.

Open or close a credit card. The reason opening or closing a credit card can immediately affect your credit is because it affects your credit utilization, a huge part of your credit score. That’s the amount of revolving debt you owe in relation to your credit limits. It’s calculated for each card and overall.

Let’s say you have one card with a $900 balance and a $1,000 limit. Your utilization is 90%, and that’s not good.

If you add a new card with a $1,000 limit, your utilization drops to 45%, which is far better.

The reverse is also true. If you start with two cards and some debt, and you close one of the cards, your utilization can skyrocket.

Change in credit utilization ratio. Some creditors change your credit limit without letting you know ahead of time (you can always opt out of a higher limit by contacting your card issuer).

If your limit goes up, your utilization will come down if you don’t add new debt.

Make or miss payments. Payment history is the single most important factor affecting your credit score. Every on-time payment helps you build a solid payment history.

Payments also affect your utilization. If you’re bringing your balances down, you can reasonably expect to see your score rise.

You may not see a big drop in your score if you pay a bill a few days late (although you could get hit with a late fee). Many creditors don’t report late payments until they’re 30 days late.

If you hit that 30-day mark and it’s a one-time issue, call the creditor and ask for the late payment to be removed from your file. Don’t expect the creditor to accommodate you more than once, though.

You will see your score suffer if you let a payment get to the 60-day or 90-day late mark.

Application for credit. A hard inquiry or “hard pull” is when a lender checks your credit report after you apply. Hard inquiries can lower your score by a few points, but your score will recover gradually over time (the inquiry affects your score for one year and remains in your file for two years).

A soft inquiry, like a self check, employer credit check, or prequalification check, does not affect your score.

When do a few points matter most?

Across the 300 to 850 spectrum, you might not think that a few points here or there would make a huge difference. But for consumers on the cusp, they do.

Poor credit consumers

The difference between poor and fair is significant, points out Beverly Harzog, a credit card expert and author of The Debt Escape Plan. Interest rates are generally highest for consumers in the “poor” category.

If you have shaky credit, focus on reaching the next threshold, especially if you’re near it. You could knock the cost of credit down and save money, especially on big ticket items.

Consumers on the cusp of any two ranges

Not all creditors will tell you the credit score ranges for their various interest rates, but some do, including most major mortgage lenders.

Let’s say you call a major bank to ask about mortgage rates. They tell you that the APR for a borrower with a 650 credit score is 4.75 percent, and the rate for a borrower with a 640 credit score is 5.75 percent. If you want to borrow $100,000, the lower credit score will cost you an additional $62 per month in interest. That’s $744 each year, and $22,320 over the life of the loan.

In other words, working to raise your credit score by just ten points could save you more than $22,000.

Economic downswings

During economic recessions, lenders tend to be more cautious when approving credit. Consumers with good to excellent credit may have more options.

What can you do to bump up your credit score?

Credit scores aren’t made of magic. Some actions have a relatively fast effect on your score (like paying off a high credit card balance), while others take time (like establishing a payment history). Generally, positive credit behavior over time will help you raise your credit score and build a solid credit file.

Pay on time every time

Pay on time. It’s the single most important factor affecting your score and should be a top priority.

Order a credit report

You can order one credit report every year from each of the three credit bureaus by visiting AnnualCreditReport.com. Check each credit report at least once a year, and hunt for errors. Not all errors are cause for concern, but some, like a collection account that you know you paid, can drag down your score. Others, like an unfamiliar address, could indicate fraud.

Get a secured credit card

If you have poor or fair credit, a secured credit card could help you build your credit score. You’ll pay a cash deposit to get the card, but then it works just like any other credit card. After six to twelve months of responsible use, you can apply for a traditional credit card and ask for your deposit back.

Check your alerts

If you’re a Credit Sesame member, read your notifications and alerts. They’ll clue you in to changes in your score, such as new inquiries and accounts or changes in your credit limits. They can also alert you to possible fraud. Your Credit Sesame membership also includes free guidance about what you need to do to improve your score, based on your own situation.

If you’re a Credit Sesame member, read your notifications and alerts. They’ll clue you in to changes in your score, such as new inquiries and accounts or changes in your credit limits. They can also alert you to possible fraud. Your Credit Sesame membership also includes free guidance about what you need to do to improve your score, based on your own situation.

Monitor your credit

The Credit Sesame free membership allows you to see your updated credit score every month, your debt, your credit utilization, your debt-to-income ratio and the progress you’ve made on all of the factors that affect your score.