We get a lot of questions from consumers about the free services we offer, and how to improve one’s credit score. Credit health and education is an important part of life, so to help you better navigate through your credit journey, we’ve gathered a list of the most frequently asked questions from our Facebook page.

Get the details of how Credit Sesame works, and sign up today.

Is Credit Sesame a scam?

Credit Sesame is a financial wellness and consumer education resource. We have appeared many times (and we don’t mean in ads) in the Wall Street Journal, the New York Times and many other respected U.S. and global publications.

Credit Sesame is a free credit monitoring service. Our site has roughly 9 million members, who take advantage of the free credit score access and other benefits we offer. We do not offer credit counseling or debt management services. We provide our members with 100% free access to their credit score, as reported by TransUnion. Your credit score is one of the most important elements of your financial life and lenders use it, along with other factors, to make credit decisions.

We also offer a vast library of educational content designed to empower consumers with the knowledge and tools they need to build an excellent, long-term credit standing.

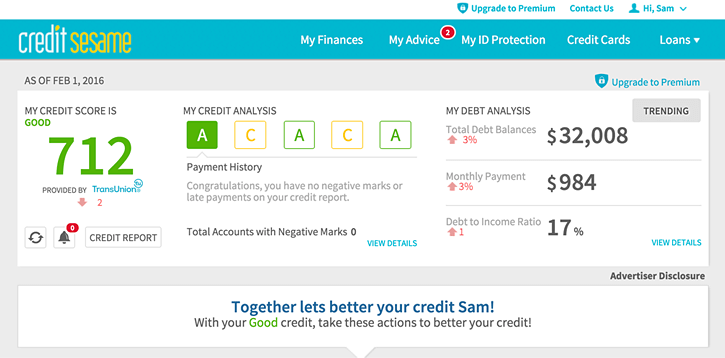

Credit Sesame members have access to their credit and debt details through a convenient and easy-to-use online dashboard that prominently features a credit report summary. On your credit report card, we tell you how you’re doing in each credit scoring factor and where you’ve got room for improvement. When you log in to view your free credit report card, you get a comprehensive analysis of your credit score and overall debt profile. For example, at a glance you’ll see your total debt balance, total monthly minimum payment and debt-to-income ratio, based on self-reported income (your income is not part of your credit report).

In your credit profile we break down the factors that are helping your score and those that could be hurting it. Credit report card grades are assigned for five specific factors: payment history, credit usage, credit age, account mix and credit inquiries. These are the factors that influence your credit score. We also show you how your credit score has changed over time.

How can we afford to offer all of these tools for free? Our business model is very simple. We earn money when we match members to financial products that are customized to each member’s credit profile. For example, if your credit score indicates that you’re likely to be approved for a mortgage at a lower rate than your current APR, we may show offers from mortgage lenders to refinance your loan. We only show you offers that could save you money and that are appropriate for a consumer with your credit profile. If you choose to click through and apply for the product, and you are ultimately approved, we earn a small commission.

Credit Sesame also provides free credit monitoring to all members. Any time your credit score changes you’ll receive an email alert in real time notifying you of the change. You can then log in and view the details to understand why your score went up or down. Keeping close tabs on your credit is especially important for consumers planning to make a major purchase, such as a home.

Credit monitoring is also a great tool for consumers who want to take a proactive stance against identity theft. Credit Sesame members receive $50,000 in identity theft insurance, along with fraud resolution assistance, absolutely free. Premium members get $1,000,000 in insurance, full monthly credit reports from all three credit bureaus, monthly credit scores from all three bureaus, 24/7 live expert support and many other benefits.

Is Credit Sesame’s credit score the same one lenders use?

Credit Sesame members receive their free credit score based on the information in their TransUnion credit profile. TransUnion generates FICO® scores, used by many lenders, and VantageScores®, which are used by at least 20 of the top 25 financial institutions in the U.S. Each lender decides which credit score to use, and which version.

The score that we offer to members is the VantageScore® 3.0. This score was developed by the three major credit bureaus—Equifax, Experian and TransUnion—as an alternative to FICO® and other credit scoring models used by commercial lenders. Like FICO®, VantageScore® uses the scoring range 300 to 850. Higher is better. Your VantageScore® is influenced by six distinct factors:

- Payment history

- Age and type of credit

- Percentage of credit limit used

- Total balance owed

- Recent credit behavior and inquiries

- Available credit

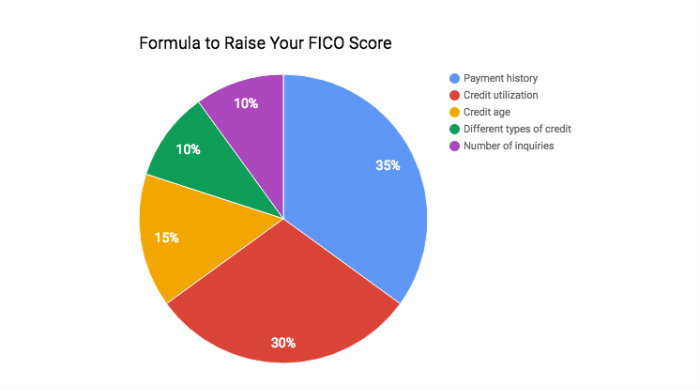

Neither VantageScore® nor FICO® shares the algorithm by which scores are calculated, but both agree that certain factors carry more weight than others. Payment history, for example, is viewed as extremely influential, but available credit is less influential.

The VantageScore® credit score factors are similar to those that FICO® relies upon. FICO® scores reflect these elements:

- Payment history

- Credit utilization

- Age of credit history

- Types of credit used

- Inquiries for new credit

In the FICO® model, payment history and credit utilization are the most important factors that influence your credit score. Late payments, delinquencies, collections and maxed out credit cards generally have the greatest negative impact on your score.

With regard to what scores lenders use, the answer depends on several variables. First, your credit score is a snapshot in time. It reflects your credit standing at exactly the moment it is calculated. It can change every time new data is reported, including the passage of time. The credit score you see today may not be the same as the credit score your lender sees next week.

Second, lenders use different scores. FICO® offers industry specific credit scores to auto lenders, mortgage lenders and credit card issuers, among others. If you have a great history with auto loans, your auto credit score might be higher than your consumer credit score. Furthermore, over time FICO® has developed multiple versions of each score. The same is true for VantageScore®. Each lender chooses whether to purchase updated credit scoring capability when new versions are released.

Credit Sesame’s Director of Operations Tony Wahl says, “Consumers should consider taking a broader view of their credit rating, rather than focusing on which credit score a particular lender may use. Because there are so many different credit scores and because consumers have no way of knowing what scoring model that a lender is going to use, consumers should use the VantageScore 3.0 that Credit Sesame provides as a benchmark to measure whether your score is improving.”

The advantage to checking your score on Credit Sesame is that it will give you a good idea of what credit score range you fall into and where you have room for improvement.

Is it completely free to sign up for Credit Sesame?

Credit Sesame is completely free to use. We don’t require a credit card number, and there is no trial period or expiration date for free memberships.

We do need your name, address, date of birth and the last four digits of your Social Security number to verify your identity and access your credit profile with TransUnion.

Credit scores are based on the data that is found in your credit report, such as your account balances, your payment history and the types of credit you use. In addition to TransUnion, Equifax and Experian also maintain credit data on American consumers. All three companies tie your credit report to your Social Security number.

Checking your credit score through Credit Sesame will not have any effect on your score. That’s because when you check your own credit, it triggers what’s known as a “soft” pull and has no effect on your score. On the other hand, when you apply for credit and the lender makes an inquiry it is a “hard” pull and generally knocks a few points from your score (temporarily). Note that for certain types of credit (mortgage, auto and student loans), you can apply with multiple lenders within a 14- to 45-day time frame but only one inquiry will count against your score.

Why is credit important?

Living on cash alone is great for the budget but not realistic for the average American lifestyle. If you want to buy a home, for example, saving enough cash to purchase it outright could take decades and many people lack the discipline to reach such a lofty long-term goal. You can buy a home sooner with a mortgage. The same goes for buying a car.

Credit is an important buffer to an emergency fund (or the lack of one). If something major happens—the car breaks down or you lose your job—do you have enough money tucked away to cover the additional expenses? With credit, you can borrow to bridge the gap. Indeed, with great credit, borrowing is often extremely inexpensive (think zero percent car loan).

To take advantage of credit, you need to have a good credit rating. Your credit score and history are essential considerations to just about every creditor. In general, a higher credit score signals that you’re responsible with credit, while a lower score indicates that you struggle to manage your finances. Lenders want to be confident that you will pay back what you borrow. They use your credit score as a gauge for how much of a risk they’re taking.

Obtaining credit is possible with a poor credit rating, but you’ll pay the price. Interest rates and fees are generally more expensive to those with bad credit, and terms are less advantageous to the consumer. (Goodbye, zero percent car loan.)

Credit Sesame’s free credit monitoring service can help you keep an eye on your credit so that you can take steps to improve your score if it’s not as high as you’d like. Using the credit report card, you can see which areas of your credit health need work. For example, if you have a grade of A for payment history but a D for credit utilization, you’ll know that you need to pay down your credit card balances, but you’re doing a great job with monthly bill payments.

Even if you don’t anticipate needing credit in the immediate future, it’s important to know your score. Stay in good credit health by practicing great credit habits over the long term. Use Credit Sesame’s free credit monitoring service to protect and improve your credit. Then, when the time comes to apply for a loan, you’ll be prepared for success.

Still got questions about Credit Sesame or credit in general? Head to CreditSesame.desk.com for more answers.