Consumers in the U.S. have not just one, but dozens of different credit scores. In a nutshell, your credit score represents a snapshot of your credit at a moment in time, and the number varies depending on who calculates it and what scoring model they use.

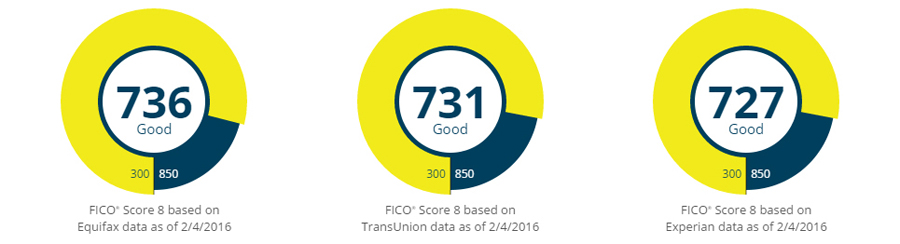

We’ll show you what that looks like using a real consumer’s credit scores gathered on a single day. You’ll see that the range is 705 to 752, and we’ll explain why that’s fine.

[See how you compare to the rest of America, when it comes to credit scores.]

The “scoring model” is the algorithm used to calculate the score. The scores shown below are based on the FICO 8 scoring model. Scoring models are complex and proprietary, and they are updated every few years.

“Our scoring model has been redeveloped several times to make sure it’s more reflective of consumer behavior,” says Tom Quinn, Vice President of Product Management for Direct to Consumer Offerings at FICO. FICO owns the scoring models most widely used by lenders in credit decisions.

The “who” is Equifax, Experian or TransUnion, the three major credit reporting agencies in the US. Since every lender doesn’t report to all three credit reporting agencies, the information in your file differs from one agency to the next, and therefore the scores they generate almost always vary slightly.

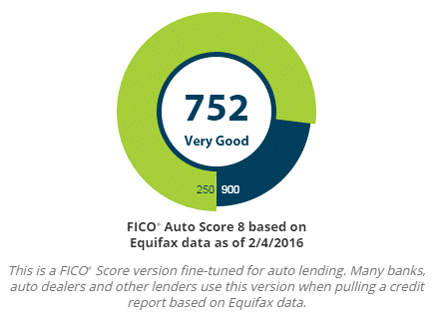

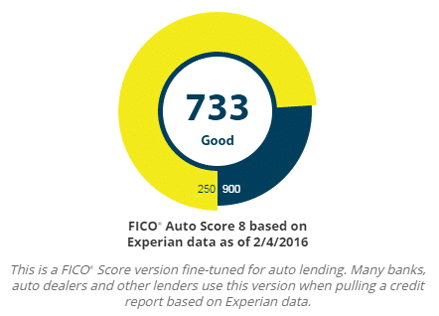

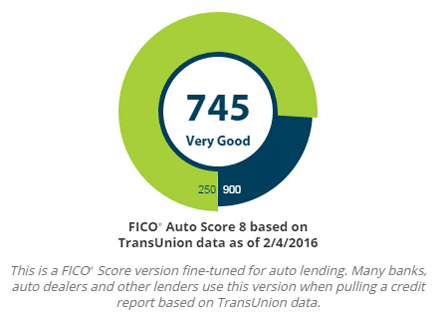

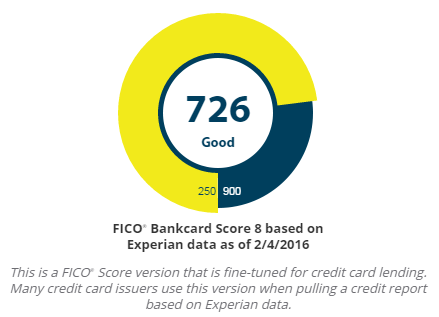

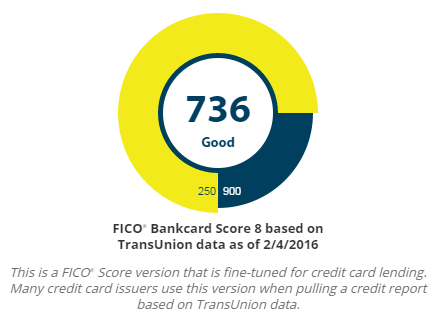

Even if the three agencies each calculate your FICO base score using the exact same algorithm, the scores will differ based on the data in your file at each agency. Take a look:

It’s important to note that even if many lending organizations still use FICO Score 8 when evaluating your credit, the credit bureaus do update their scoring methodologies every few years. As of 2020 Fair Isaac Corporation is rolling out FICO Score 10.

What is VantageScore?

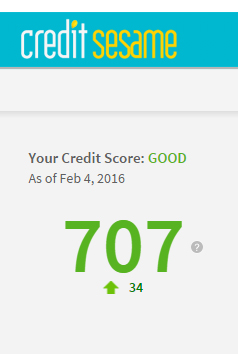

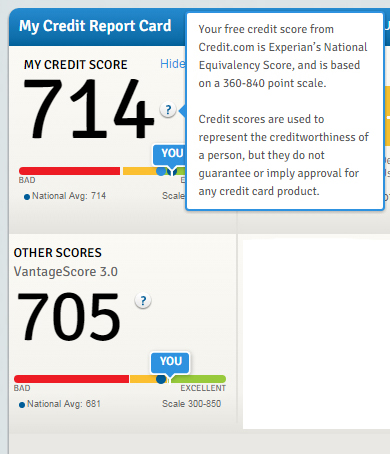

The credit scores you see on Credit Sesame and other free credit score sites and on your bank website or credit card statement may not be exactly the same as the score a lender sees when you apply for credit. Here’s the same consumer’s Credit Sesame score on the same day:

Why is it different? Credit Sesame offers the VantageScore 3.0, provided by TransUnion. This VantageScore 3.0 score is based on whatever data is in the consumer’s TransUnion credit file on the day it’s calculated.

VantageScore was developed by the three big credit reporting agencies – TransUnion, Equifax and Experian – to compete with FICO. VantageScore is now used by more than 2,000 lenders nationwide, including 7 of the 10 largest banks.

[Related: Rent & Utilities to Be Stronger Factors for Your Credit in 2016?]

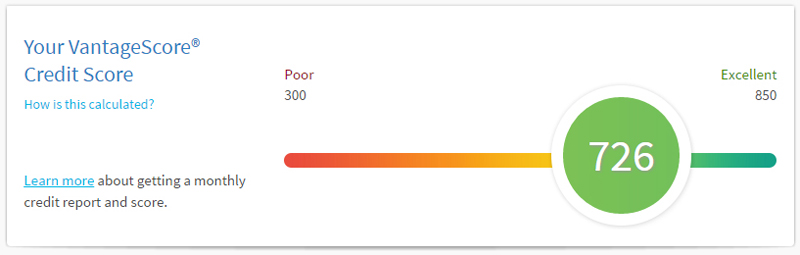

Like FICO, the VantageScore ranges from 300 to 850. (Earlier VantageScores ranged from 501 to 990.) VantageScore uses a different algorithm to calculate credit scores that it claims more accurately predicts credit risk.

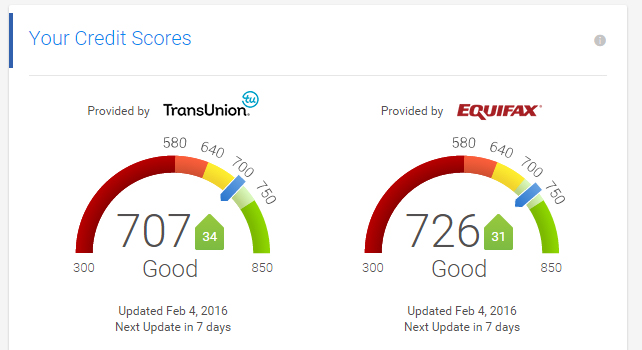

Credit.com, Credit Karma, LendingTree, myBankrate, MyCreditCards.com, Quizzle and WalletHub all also offer the VantageScore 3.0 score for free, provided by TransUnion, Equifax or Experian.

Again, scores for the same consumer on the same day, on various free credit score websites:

FICO and VantageScore both offer specially tailored versions of your credit score to different types of creditors, including lenders in the auto, mortgage and real estate industries. Those industry scores may differ slightly from the base version of your score.

Mortgage credit scores

When you apply for a mortgage, the lender gets a special credit report that shows data from all three credit agencies. The report is called a “merged” report, or a residential mortgage credit report (RMCR), and it allows the lender to see the most complete picture of your credit possible. This report is more comprehensive than the credit report other types of lenders see.

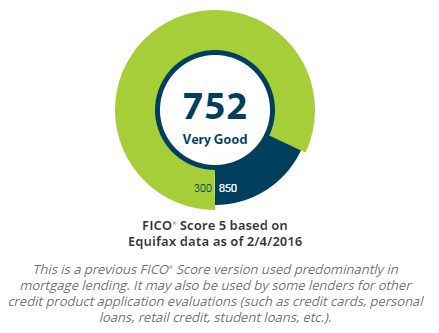

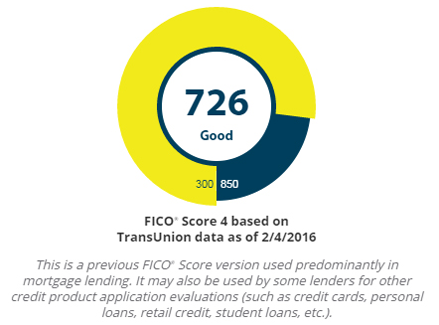

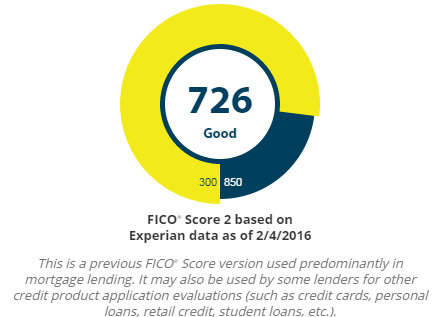

The mortgage lender will also see three different FICO scores from the three credit agencies, and they’re all based on different FICO scoring models. The Equifax score is based on FICO 5, the TransUnion score is based on FICO 4, and the Experian score is based on FICO 2. All of these are tailored to predict the likelihood that you will repay your mortgage. The data is analyzed in such a way to determine whether “there is something that makes this consumer more or less risky for that industry,” says Quinn.

The mortgage lender might base its approval (and interest rate) decision on the middle score, or it might take an average of the three.

Auto credit scores

Auto lenders use a FICO or VantageScore that is specially tailored to predict the likelihood that you will repay your auto loan. This industry score gives greater weight to your history with auto loans and other, similar installment loans.

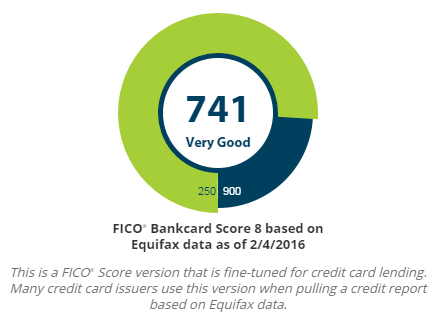

Bankcard credit scores

For credit card issuers, FICO and VantageScore offer specially tailored bankcard credit scores that are designed to predict how risky you are with credit cards and other revolving credit.

The interesting thing, though, is that the credit card account approval process varies widely. Credit card issuers are more secretive and don’t reveal their underwriting guidelines or which score they intend to pull for a given application.

Indeed, an issuer might pull one applicant’s credit report summary and score from one agency, and another applicant’s report and score from another agency. Most also perform an in-house credit analysis, particularly when the customer applies for a credit line increase.

Which credit score is most important?

The truth is that all of these credit scores are accurate reflections of the consumer’s credit risk, and vary depending on the information in the consumer’s file and the data the score aims to emphasize. Taken as a group, these scores show that the consumer has decent credit, but there’s plenty of room for improvement.

[You May Also Like: Why You’ll Feel Better About Your Low Credit Score When You Tackle This First]

Rather than focusing on the numbers, focus on ways to improve them. The very same actions will improve the scores across the board. “What’s important for the consumer is not all [of the different] FICO scores, but to think about their goal, and to try to understand their score and report,” says Quinn.

[Related: Understand Lender Credit Lingo & Jump to a Higher Credit Category]

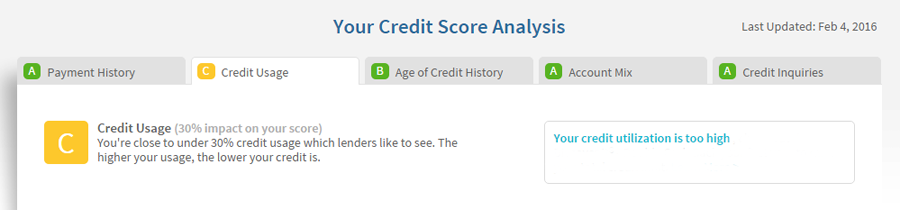

No matter where you view your credit score, pay close attention to the factors holding it down and suggestions for bringing it up. In our consumer’s case, the highest priority is to get revolving balances paid down.

Reviewing Credit Sesame’s letter grades for the different factors affecting this consumer’s credit score, we can see that average account age is the second priority. Our guy can move from a B to an A by avoiding opening new accounts, and keeping old accounts open and in good standing.

[Related: How to Move Your Credit Grade From a ‘C’ to ‘B’ in 2 Simple Steps]

Once he achieves straight As across the board, we won’t be surprised to see this consumer’s score jump past 800 no matter what agency calculates it!