Your credit plays a bigger role in your overall financial well-being than many people realize. Your credit score and your credit report are seen as markers of your responsibility with money — and ones that nearly all lenders and financial institutions take seriously. Whether you’re looking to buy a car or a house, start a business or even get that dream job, a strong credit score will take you a long way toward realizing your goals.

As you’ll see in the graph below, more than half of the American population has a credit score that is considered fair, poor, or very bad. If your credit score falls in one of these categories, know that you’re not alone. In fact, you’re with the majority of Americans and, good news — there are easy steps you can take to help improve your score in a matter of months.

Comparing Credit Score Ranges of Credit Sesame Members

| Score Range | Value Range | Members |

|---|---|---|

| Poor Credit Score | 580 & Below | 45% |

| Fair Credit Score | 581 - 669 | 32% |

| Good Credit Score | 670 - 739 | 14% |

| Very Good Credit Score | 740 - 799 | 6% |

| Excellent Credit Score | 800 & Above | 3% |

Source: Credit scores were calculated from 5,000 Credit Sesame members in November 2019.

Introduction

You’re not alone if you’re trying to improve your credit and understand credit repair. While the average American credit score is reaching new highs — certainly a good sign— plenty of people are still actively working not only to increase their understanding of repairing their credit, but to do it in as smart and solid a way as possible.

If you are someone who wants to increase your credit, keep reading. We’ve prepared a step-by-step guide for you.

Why is Credit Repair or Fixing Your Credit Score Important?

First off, it’s crucial to know your score so that there are no surprises when the time comes to apply for credit. Items can also stay on your report longer than you might think, affecting you for years down the line.

The chart below shows just how long a negative item can stay on your report and the average credit score drop that it can have. A late payment, for example, stays on for 7 years and can drop your score more than 35 points! If you have one on your credit report, there is nothing you can do about that, but there are things you can do to ensure it does not happen in the future.

How long do negative factors stay on your credit report?

| Negative Factor | Max. Time on Credit Report | Avg. Credit Score Drop |

|---|---|---|

| Late Payments | 7 Years | 35 |

| Charge-Off | 7 Years | 69 |

How to Fix Your Credit Score

Here are the steps you can take to fix your credit:

1. Pinpoint your credit score killers

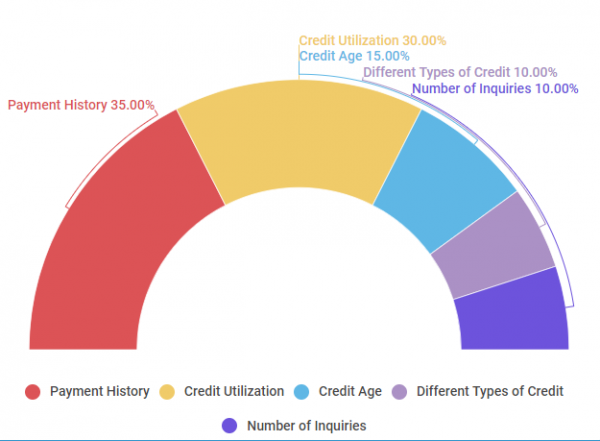

While your credit score may seem like a complicated, arbitrary number, it is actually calculated based on five core factors: your payment history, credit utilization, the age of your credit accounts, the mix of your credit accounts, and your history of applying for credit. They are not equally weighted, and this information can be slightly different among the various credit bureaus.

FICO scoring model calculation (weight) factors

| Credit Factors | Credit Score Weight |

|---|---|

| Payment History | 35% |

| Credit Utilization | 30% |

| Credit Age | 15% |

| Different Types of Credit | 10% |

| Number of Inquiries | 10% |

Source: https://www.myfico.com/credit-education/whats-in-your-credit-score

Taking a closer look at these factors will tell you what is hurting your score… but where do you go from there? Since one of the fastest ways to see an improvement in your credit score is to fix any errors on your credit report, that’s your next step.

2. Clean up your credit report

Request a copy of your credit report from all of the credit bureaus. If you see any errors, it is important that you start the dispute process as soon as possible. Credit reporting agencies will then have 30 days to respond to your dispute. If you receive unfavorable results from the credit reporting agencies, you can either appeal the decision, or dispute the item directly with the creditor listed.

3. Start some positive credit history

Once you’ve done your best to mitigate and lessen any previous negative factors on your credit report, it’s important to start building some positive credit history right away. Perhaps you’ve been denied a credit card or a certain type of credit in the past. Fortunately, this doesn’t mean that you’re entirely shut out from borrowing and building credit. Consider a secured credit card, which will require a deposit that becomes your credit limit. If you fail to make payments, the company can then withdraw the funds from your account automatically. Lenders are much more lenient extending this type of credit, and it can be a fantastic way to start the credit repair process.

| Free credit score |

|---|

| Credit repair |

| how to fix your credit |

| how to increase your credit score |

| Whats the highest credit score |

| Excellent credit score |

The Key Points: A Closer Look at Credit Repair

According to our research, 13 percent of Americans have tried credit-repair agencies. You may be wondering how they work. Here’s how.

Essentially, credit-repair services work to remove negative items such as judgments, liens, foreclosures, bankruptcies, and late payments from your record. They do this by getting your report from all three agencies — Equifax, TransUnion, and Experian — and identifying disputable items in each. They then file disputes on this information, and stay in communication with the agencies until the item is removed.

Unfortunately, not all companies are completely focused on helping you, so you need to be careful to avoid credit-repair scams. Also, not all information can be disputed, and the information that can be, you can do yourself by following these steps. This includes being proactive with your own due diligence and carefully reading any and all contracts before signing.

Also, be aware of the following rules for credit-repair companies as set forth by the Credit Repair Organizations Act:

-

- They may not charge a fee until they fully complete the promised services

- They must provide a written contract

- They can’t advise you to mislead any bureau or alter your identity

- They can’t ask you to sign anything that requires you to give up your rights under the Credit Repair Organizations Act.

How Long Does it Take to Repair Your Credit

Now that you’ve learned some of the steps to repairing your credit, let’s take a look at how long it can take for this process to work. Each individual is different, and therefore each individual credit score is as well. What works for one may not work for another, but using general lessons as guidelines, everyone can see an increase in their credit score. The chart below shows the average length it takes to increase credit scores by doing a variety of things. The average time it takes to go from poor credit to fair credit is roughly 65 days.

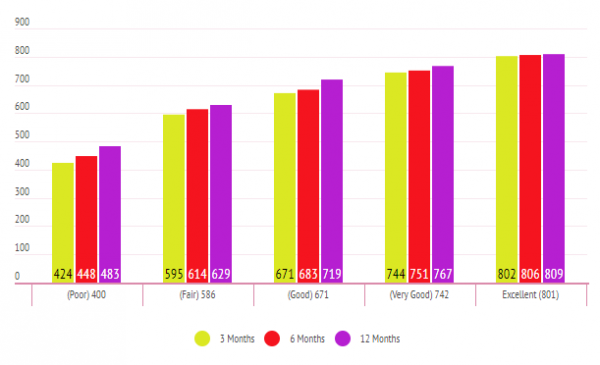

Improving Your Payment History and Credit Utilization

First, let’s look at how paying your bills on time affects your score. As you can see, if you begin with a score under 600 and pay all your bills on time, you score can improve 10-15 points in just one month.

Average Credit Score Improvement making payments on time

| Credit Starting Point | 3 Months | 6 Months | 12 Months |

|---|---|---|---|

| (Poor) 400 | 424 | 448 | 483 |

| (Fair) 586 | 595 | 614 | 629 |

| (Good) 671 | 671 | 683 | 719 |

| (Very Good) 742 | 744 | 751 | 767 |

| Excellent (801) | 802 | 806 | 809 |

Source: Review of 600 individuals who for the course of a year made all payments on time. The study was conducted in February of 2016 and concluded April of 2016.

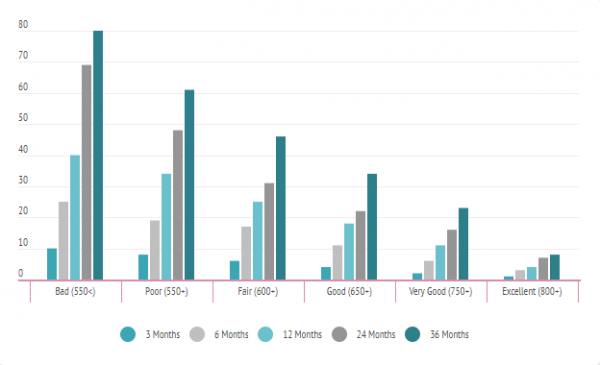

Now let’s take a look at how improving your use of credit can affect change in your score, as well as the amount of time it will take to see a change. Keep in mind that these are rough figures and will vary with each individual situation — but this will give you an idea of what you may be facing.

Average increase to credit score by decreasing credit utilization below 30%

| Credit Starting Point | 3 Months | 6 Months | 12 Months | 24 Months | 36 Months |

|---|---|---|---|---|---|

| Bad (550<) | +10 | +25 | +40 | +69 | +80 |

| Poor (550+) | +8 | +19 | +34 | +48 | +61 |

| Fair (600+) | +6 | +17 | +25 | +31 | +46 |

| Good (650+) | +4 | +11 | +18 | +22 | +34 |

| Very Good (750+) | +2 | +6 | +11 | +16 | +23 |

| Excellent (800+) | +1 | +3 | +4 | +7 | +8 |

Source: Review of 600 individuals who for the course of a year who maintained a 30% or lower credit utilization. The study was conducted in February of 2016 and concluded August of 2018.

Age of Credit History and Types of Accounts

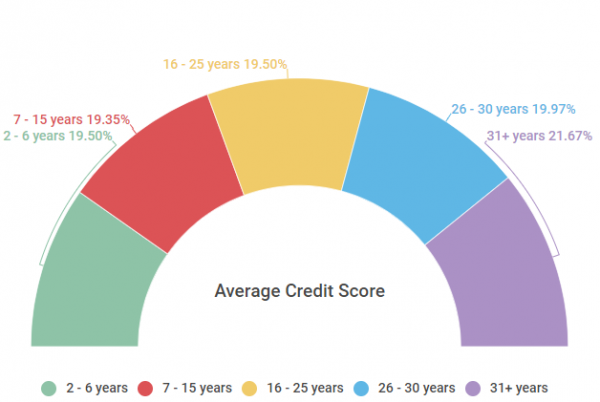

Longer credit histories typically, though not always, can mean improved scores. What it does show to prospective creditors is that you are able to manage lines of credit in a responsible manner for a significant amount of time. Note that when creditors receive your credit report, it does not just show length of account, but average balance, as well as how often payments are late or missed. The graph below looks at the age of your credit history versus the average score for that amount of time.

Credit Age versus Average Score

| Credit Age | Average Credit Score |

|---|---|

| 2 - 6 years | 630 |

| 7 - 15 years | 625 |

| 16 - 25 years | 630 |

| 26 - 30 years | 645 |

| 31+ years | 700 |

Source: We surveyed 1,000 Americans on the age of their credit accounts vs. their credit score.

When improving your credit, it’s important to consider the types of accounts you will open as they reflect strongly upon your credit. Before you run to open a new account, ensure that you are financially able to pay for anything you borrow. A variety of accounts will not help your credit score if you have missed payments or high credit utilization as a result. Below you’ll learn more about about this

Credit Score Improvements Through Diversifying Credit Accounts

| Credit Ranking | 1 credit type | 2 credit types | 3 credit types | 5+ credit types |

|---|---|---|---|---|

| Bad (550<) | +8 | +14 | +17 | +42 |

| Poor (649<) | +7.5 | +12 | +15 | +36 |

| Fair (699<) | +6.9 | +11 | +15 | +34.4 |

| Good (749<) | +6.6 | +10.6 | +14.3 | +30.8 |

| Very Good 750>) | +2.1 | +5.1 | +11.1 | +19 |

| Excellent (800>) | +1.6 | +1.9 | +3.2 | +4.5 |

Source: Credit Sesame surveyed 600 Americans on how their credit scores improved with the addition of new financial products. Participants were divided by credit ranking and further categorized by the number of financial products they possessed (credit cards, merchant credit cards, car loans, and mortgage loans). The study was conducted August 2015 and concluded August 2017.

Benefits of Learning How to Fix Your Credit

There are a number of practical benefits to repairing your credit:

- You’ll get faster approval on any loans

- It will be easier to purchase a new home

- If you rent, you’ll be more likely to be able to rent the place you want

- It will be easier to get a new car

- You can get better terms on your credit cards

TLDR; why should you care about fixing your credit score

Credit is an essential part of modern-day American life. It’s important to know how to build, maintain — and if necessary, repair — it. Follow these steps and you’ll be on your way to a better credit score in no time.