The allure of credit cards is that they allow us to buy things we can’t afford right now and pay for them later. We can charge what we want and pay off the balance at our leisure. But unless you take advantage of a temporary offer, you’ll pay a price for the privilege of using a bank’s money to buy what you need. That price takes the form of interest charges levied on the balance owed. Making minimum monthly payments — versus paying off the balance in full at the end of every month — could end up costing you a lot more than you might think.

[cta button=”text for button” image=”http://override-default-image-url” link=”http://override-default-link/”]Check Your Free Credit Score — No Credit Card Required![/cta]

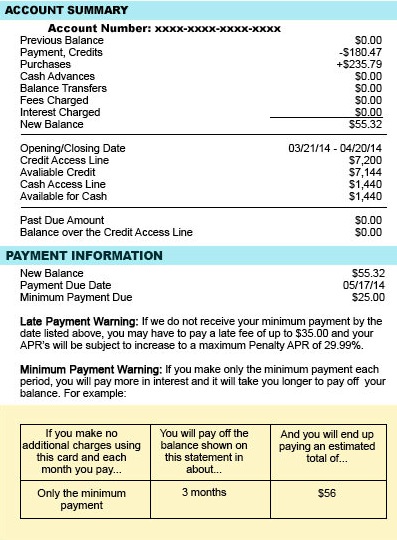

The Minimum Payment Warning box is a little box that now appears on all credit card statements. It tells you in very simple terms how long it will take you to pay off your credit card balance by making the minimum payments only. In example #1 below, the the warning box is highlighted in yellow.

Example #1:

In example #1, the balance is quite low. If a financial emergency exists and this consumer can’t afford to pay off the charges immediately, the cost is minimal to spread it out over a few months (less than one dollar). The larger problem comes with higher balances. Now look at example #2.

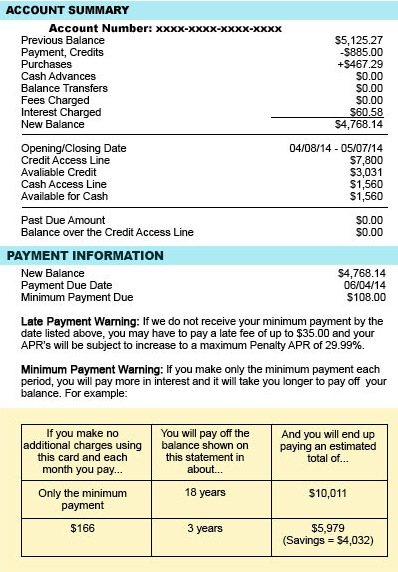

Example #2:

This consumer has a balance of nearly $4,800. The warning box clearly shows that if he makes only the minimum payment each month, he will pay more than $10,000 over the course of 18 long years. The true cost of minimum payments, therefore, is over $4,000 in additional interest charges and 15 years of monthly payments. Notice that increasing the payment to just $166 and keeping it at that amount until the balance is paid cuts the life of this debt down to just three years. The difference is mind-blowing.

Diminishing minimum payments

The forever nature of minimum payments is due to the fact that in addition to being a tiny percentage of the balance owed, as the balance goes down, so too does the required minimum payment. Any consistent increase in the payment amount will noticeably – even drastically – shorten the life and total cost of the debt. For example, if the cardholder can afford to stick to the current payment amount of $108, the debt will be paid off within about six years. You don’t have to do the math in your head if you want to play around with the numbers. Search online for “credit card repayment calculator” and enter your details. Here’s a nice one provided by State Farm.

“Can I afford that?”

If you are considering a purchase that you can’t afford to pay off completely right now and you’re tempted to charge it, look at this true cost calculator first. The credit card accounts illustrated above are at 15.24 percent interest. The iPod Touch 64G costs $399. If this consumer wants one and can only afford to pay $25 per month toward the balance, he’ll spend 18 months paying it off and the iPod will ultimately cost him about $450. If his minimum payment is just $15, he can stretch it out to 32 months and pay about $490 for that iPod. Indeed, many credit cards require a minimum payment of just two percent of the balance (usually not lower than $10). In that case, our iPod buyer can take a full 57 months (that’s 4.75 years) to pay off his purchase, for a total cost of $564, or 41 percent more than the original purchase price). Is the item you want worth that much more?

More on Credit Cards:

- Top Credit Card Dangers (and How To Protect Yourself From Them)

- Credit Card Traps Buried in the Fine Print

- The Secret to Getting Out of Credit Card Debt: 0% Balance Transfer

- Why Don’t My Credit Cards Ever Show a Zero Balance on My Credit Reports?

- 5 Credit Card Perks You May Not Know You Have

- 5 Pitfalls of Reward Credit Cards