Credit Sesame explains why many consumers lose more and gain less when interest rates rise.

In theory, when interest rates rise, some consumers benefit while others suffer financially. However, a recent study found an imbalance. On average, rising interest rates have cost American consumers more than they’ve benefited.

Net interest earnings dropped as interest rates rise

Consumers earn interest on savings accounts and other interest-bearing products. In contrast, consumers pay interest on loans and credit card balances. When rates rise, consumers with more savings than debt should benefit from interest earnings. Consumers with more debt than savings should lose out because of increased interest payments.

A study by the Bureau of Economic Analysis found that this trade-off has worked against consumers overall as rates have risen over the past couple of years. Since the Fed started raising interest rates in early 2022, the total interest consumers pay on credit cards and loans rose by $420 billion. Meanwhile, the total interest they earn on savings has increased by just $280 billion. This interest earnings/payments disparity means consumers have lost out to the tune of $140 billion.

Why have rising interest rates worked against consumers?

There are a couple of market forces that have really tilted the playing field against consumers.

The Fed plays a prominent role in setting interest rates. However, when it comes to the rates offered to consumers, decisions by financial institutions have an important impact. Consumer choices have also contributed to the rising interest charges Americans are paying.

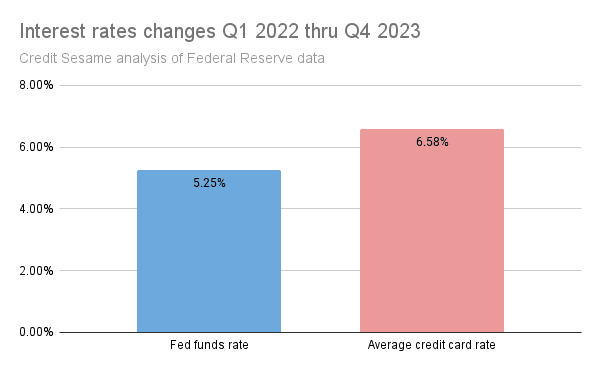

Credit card rates have risen faster than the Fed funds rate

An example is credit card rates. Credit card rates have risen more than the Fed funds rate over the past couple of years.

The Fed started raising rates late in the first quarter of 2022 and has since increased the Fed funds rate by 5.25%. The average rate charged on credit card balances has risen even more over the same time. It is now 6.58% higher than in the first quarter of 2022.

Credit card interest has risen more quickly than the Fed funds rate partly because lending money to consumers has become riskier. Late payment rates on credit card accounts have risen, and so have credit card balances.

Consumers carry more debt in credit card balances

Rising credit card balances also impact why consumers are paying more interest. Credit card interest rates are generally much higher than rates on other major forms of credit, such as car loans, mortgages, and personal loans. The more of your overall mix of debt you have in credit card balances, the more interest you’re likely to pay.

Over the last few years, credit card balances have been representing a rising percentage of total consumer debt. According to figures from the Federal Reserve Bank of New York, from the first quarter of 2021 through the end of last year, credit card debt as a percentage of total consumer debt rose from 5.26% to 6.45%.

With consumers now keeping more of debt in high-interest credit card balances, it’s no surprise Americans are paying more interest.

Deposit rates have not kept up

In addition to the interest consumers pay on their debt, there’s another side to the net interest equation. Consumers earn interest on their savings that may offset what they pay on their debts. Unfortunately, average rates on deposit accounts haven’t come close to keeping up with the average rates charged on consumer debt.

According to figures from the FDIC, since the Fed began raising interest rates in March 2021, the average interest rate offered on bank savings accounts has risen by just 0.43%. The average rate offered on 5-year CDs has risen by just 1.07%.

Those numbers are a far cry from the 5.25% increase in the Fed funds rate over the same period, let alone the 6.58% average increase in credit card rates.

How consumers can improve their net interest

To improve their net interest earnings, consumers need to take matters into their own hands. Here are four things you can do to improve your net interest:

- Reduce debt balances. This is an especially expensive time to be carrying debt, so reducing debt can be especially rewarding right now.

- Choose cheaper forms of debt. Only use credit cards for purchases you can pay off within a few months. If you need more time to pay, take out a loan with a lower interest rate—or consider delaying the purchase while you save up for it.

- Shop for a better rate. Whether you’re looking for a credit card or a loan, there may be a better deal out there. Interest rates vary widely from one financial institution to another, so shopping around is well worth the time.

- Work to improve your credit score. Loans and credit cards for poor credit customers charge much higher rates than those for people with good credit. Credit score improvements can affect your net interest earnings and thus help you build your net worth.

If you enjoyed Do you win or lose when interest rates rise? you may like,

- Interest rate increases are not a windfall for savers

- 5 things to do as interest rates rise

- How to build credit

Disclaimer: The article and information provided here are for informational purposes only and are not intended as a substitute for professional advice.