Credit Sesame analyzes the effect of inflation on retirement savings.

Saving for retirement is tough enough under normal circumstances. Inflation makes it even harder. Retirement may seem a long way off, but the threats that inflation poses to your retirement security have to be faced now. Otherwise, inflation can put you way behind your retirement savings schedule. Perhaps so far behind that you never catch up.

How does inflation threaten your retirement savings? What can you do to minimize the effect?

Moving the goalposts: Inflation raises retirement assumptions

Retirement planning is centered around understanding how much money you need for a comfortable retirement. You may set a goal of the sum you need to have accumulated by the time you retire to maintain the lifestyle you want. Inflation can change things. It can make the target easier to reach (if inflation goes down) or harder to reach (if inflation goes up).

A key factor in setting a retirement savings target is an inflation assumption. You start by figuring out what your retirement living expenses would be if you retired now. Then you adjust those expenses for what they are likely to be by the time you retire, which might be decades down the road.

High inflation shakes up assumptions

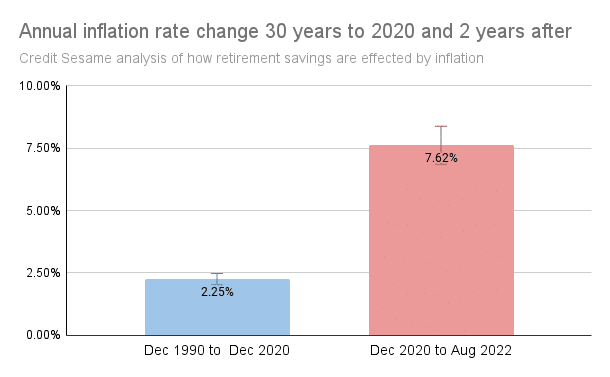

Retirement calculators and other planning tools adjust those expenses based on an assumed inflation rate between now and when you retire. Until recently, the United States enjoyed thirty years of unusually low inflation. Since the end of 2020, that has changed drastically.

The numbers in this chart are based on Consumer Price Index data from the Bureau of Labor Statistics. From the end of 1990 through the end of 2020, the inflation rate averaged 2.25% a year. That’s very mild inflation by historical standards.

Things have been totally different since the end of 2020. Since then, inflation has risen at an annual pace of 7.62% a year.

The period from 1990 through the end of 2020 was such a long period of low inflation that it might have led people to underestimate future inflation. A low inflation assumption when calculating your retirement target can cause you to come up short.

The dollar impact of high inflation on retirement expenses

Seeing percentage rates on a page doesn’t always drive home just how big a difference a change in the inflation rate can make. To get a clearer idea of the impact high inflation can have on your retirement expenses, it helps to look at it in dollar terms.

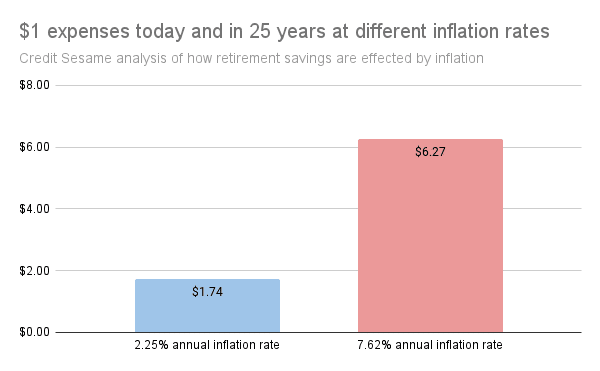

The chart below uses an example of someone retiring in 25 years. It shows what would happen to a dollar’s worth of today’s expenses by then under two inflation scenarios: the mild inflation of the 1990 – 2020 period, and the high inflation we are now experiencing.

If you assume inflation continues at the low rate of the 1990 to 2020 period, in 25 years, it takes $1.74 to cover the equivalent of $1 of expenses today.

However, if inflation continues at the rate it has maintained since the end of 2020, in 25 years it takes $6.27 to cover those same expenses.

If high inflation continues, retirement is going to become a lot more expensive. Inflation is unlikely to continue at the high rate of the past couple of years but, longer term history suggests inflation is likely to be higher than during the 1990 to 2020 period. Or anywhere in-between.

Because of this, you might want to look at using a higher inflation assumption in your retirement planning calculations. Doing that raises your retirement savings target. This makes that target tougher to meet, but means you are more likely to have adequate or excess funds on retirement.

Maintain retirement plan contributions

Inflation creates immediate demands that make it hard to think about the future. When you’re struggling to make ends meet, it takes a lot of discipline to continue to make your full retirement plan contributions.

However, this is the wrong time to cut retirement contributions in order to fund your current lifestyle. Remember, inflation may mean you need to save more for retirement, not less.

Also, if you participate in a plan that matches some or all of the contributions you make, you leave money on the table if you reduce your contributions.

It may take some sacrifice to cut your spending rather than skimp on your retirement contributions. However, if you don’t save enough for retirement, even bigger sacrifices may be forced upon you in the future.

Avoid using your retirements savings as a piggybank

It’s bad enough that inflation causes some people to reduce their retirement savings. What’s even worse is if they start dipping into retirement savings early to meet current expenses.

When you struggle to pay the bills, it’s understandable that dipping into your retirement savings may seem attractive. The money is there, it’s yours, so why not use it to meet a pressing need?

The problem is, using retirement money early is very costly. If you withdraw from your retirement savings before you reach retirement age, you pay a 10% penalty on top of any ordinary income taxes due on the withdrawal.

Even if your plan allows you to borrow against your balance, there may be costs involved. As long as the money is out of the retirement plan, you miss out on any investment returns you could have earned. If you lose or quit your job, your plan might require you to repay the loan immediately.

Have faith in your investments

Investments are having a bad year. Higher costs squeeze corporate earnings. Rising interest rates drive down bond prices. They make other investments, from stocks to cryptocurrencies, less attractive.

It takes a certain amount of faith to keep investing when the returns aren’t good. Ultimately though, sticking to an investment plan in good times and bad may be your best shot at growing your savings enough to meet your retirement needs.

Meeting these challenges means thinking ahead

You need to worry about retirement now. High inflation makes it urgent to adjust your retirement savings now. Retirement planning should be as high a priority as your current expenses. This may make coping with inflation even harder now, but it should pay off in the long run.

You may also be interested in:

Disclaimer: The article and information provided here is for informational purposes only and is not intended as a substitute for professional advice.