Credit Sesame discusses bond vigilantes, what they do and how they may combat inflation.

In the 1970s, there was a bit of a fad for vigilante movies. Films like Death Wish and Walking Tall highlighted the idea of a lone man resorting to extraordinary means to right the wrongs of society.

In the 1980s, a less violent but extremely effective vigilante emerged. They were nicknamed “bond vigilantes,” and the enemy was inflation.

It is worth looking back on this era because bond vigilantes appear to have returned. The good news is that they may help in the battle against inflation. The bad news is that in the process they may have a damaging impact on your borrowing costs, economic growth and investments.

What are bond vigilantes?

The phrase “bond vigilantes” does not refer to a specific group of people. Instead, it refers to a type of behavior that is evident in the bond market from time to time.

The nature of most bonds is that they promise a fixed payout over the life of a bond. This can provide a form of security. You can buy into a bond knowing what interest payments you will receive regularly and how much principal you will receive when the bond matures.

If it’s a high-quality bond, like one issued by the U.S. Treasury, the only real threat to this security is inflation. Inflation erodes the purchasing power of those future interest and principal payments. If the inflation rate rises above the yield on your bond, your investment will lose purchasing power over time.

As a result, bond investors tend to be very sensitive to signs that government policies or economic trends are becoming too inflationary. Under these conditions, bond investors may react swiftly and decidedly when they see any hint of further inflation. They do this by selling their bonds en masse.

These sell-offs cause bond prices to plunge. When that happens, bond yields – akin to interest rates – rise. This is one way the economic system self-corrects when inflation gets too high. A sharp rise in interest rates chokes off economic growth by raising borrowing costs, causing inflationary pressure to ease.

There’s a mistaken belief that the behavior of bond vigilantes is a form of protest against certain fiscal or monetary policies. While it may seem that way, sending a message is not what bond investors have in mind when they start selling. They are just protecting themselves when high inflation threatens the value of their investments.

Bond vigilantes in the early 1980s

This happened in the early 1980s when the phrase “bond vigilantes” emerged. As inflation rose in the late 1970s and early 1980s, investors began to flee the bond market. This exodus peaked in September of 1981 when 10-year Treasury yields reached a high of 15.84%. This was far above their 50-year average of 5.98% and well above the Fed funds rate at the time which was 10.59%.

This was important economically because while the Fed funds rate directly impacts short-term lending to banks, Treasury yields have more in common with long-term rates like mortgage rates and corporate bonds. Also, Treasuries are traded every day, so they can react more swiftly than the Fed, which meets ten times a year.

In the early 1980s, the spike in Treasury yields had a brutal impact on the economy and the job market. Rising bond yields helped send the economy into a recession that lasted for 16 months. During that recession, the unemployment rate reached 10.8%.

Still, for all the negative impact on economic growth, the surge in bond yields did help to tame inflation. The year-over-year increase in the Consumer Price Index peaked at 14.6% in 1980. By mid-1983, it was down below 3%.

The willingness of the bond investors to take extreme measures to tame inflation earned them the nickname “bond vigilantes.”

Have bond vigilantes returned?

When inflation started rising in 2021 and 2022, bond investors were slow to react. There was a general belief that the flare-up of inflation was just a temporary reaction after pandemic lockdowns. At first, this left the inflation-fighting job primarily to the Federal Reserve, which began raising interest rates in early 2022. By early 2023, the Fed funds rate had risen above Treasury bond rates, though both still trailed inflation.

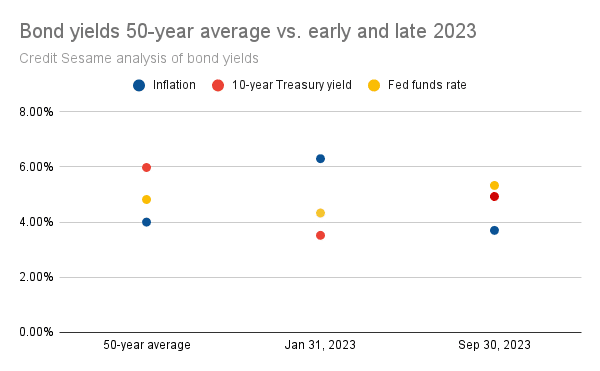

The first column of dots in this chart shows the 50-year averages for 10-year Treasury yields, the Fed funds rate and inflation. Historically, Treasury yields have been more than a full percentage point above the Fed funds rate, and both have been comfortably above inflation. By early 2023, these relationships had been turned upside down. Inflation had leaped well ahead of the Fed funds rate, and Treasury yields trailed even further behind. However, over the past several months to the end of September 2023, things have begun to normalize. The Fed funds rate has gotten ahead of inflation. Treasury yields have risen even faster than the Fed funds rate, which has allowed them to surpass inflation and close the gap with the Fed funds rate.

What this means for rates and consumers

The surge in Treasury yields means that bond investors recognize that inflation is proving to be more stubborn than originally thought. Inflation has come down somewhat but remains far above the Fed’s 2% target. A variety of economic forces lately have turned the inflation trend back up. The rise in bond yields since the end of August 2023 means that effectively, the bond market has joined the Fed in the fight against inflation. Bond investors are now wary enough of inflation that they are demanding higher yields before they put their money into the market. Bond vigilantes are back.

Long-term bond yields have more in common with long-term loan rates than the Fed funds rate does. Notably, the recent rise in bond yields has been accompanied by a rise in mortgage yields. Besides home buyers, governments and corporations will have a harder time borrowing due to higher long-term rates. That discourages spending and takes some fuel away from the inflationary fire.

As in the early 1980s, the surge in bond yields may help bring inflation under control. However, the price to be paid for the help of bond vigilantes may be a period of high interest rates and slow growth.

If you enjoyed The return of bond vigilantes you may like,

Disclaimer: The article and information provided here is for informational purposes only and is not intended as a substitute for professional advice.