You’ve learned you have a 614 credit score. What does that mean? Is a 614 credit score good or bad, or somewhere in between? Can you expect anything from lenders with that score? And if so, what does it mean? Let’s take a closer look at this particular score:

What can you do with a 614 credit score?

For the purpose of this article, we’re going to look at the FICO Score model for credit scores, since it is the most widely used and known model. FICO Scores are three-digit scores that fall somewhere between 300 and 850 — the higher your score is, the better your credit is. On the FICO scale, 614 is considered to be Fair credit, but there are plenty of lenders who will extend credit to people with scores in this range. Consumers with this credit score can, however, be considered poor borrowers, and may be subject to higher interest rates or less than ideal terms for loans and/or credit cards.

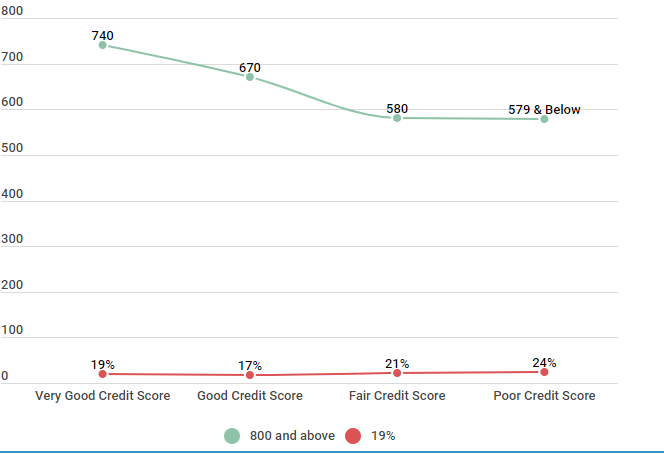

Comparing Credit Score Ranges of Credit Sesame Members

| Score Range | Value Range | Members |

|---|---|---|

| Excellent Credit Score | 800 and above | 19% |

| Very Good Credit Score | 740 - 799 | 19% |

| Good Credit Score | 670 - 739 | 17% |

| Fair Credit Score | 580 - 669 | 21% |

| Poor Credit Score | 579 & Below | 24% |

Source: Credit scores were calculated from 5,000 Credit Sesame members on 2/6/18.

If your credit score isn’t where you want it to be, don’t fret — there are steps that you can take to help build and improve your credit. But before you can know how to improve your score, you need to first understand the individual factors that contribute to your score.

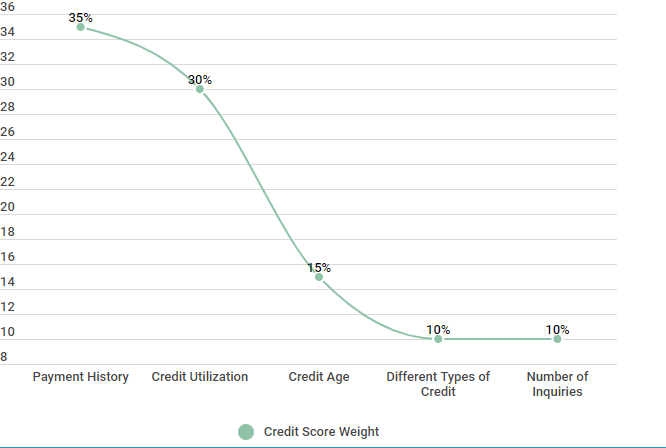

Factors in your credit score

In order to fully understand your credit score, let’s take a closer look at what goes into building your score.

- Payment History. Your payment history accounts for 35 percent of your total score, making it the single most important factor. The best thing you can do for your credit score is to make at least your minimum payment due on time each month — every month.

- Credit Utilization. Your credit utilization isn’t far behind your payment history when it comes to weight. Accounting for 30 percent of your credit score, your credit utilization can most simply be thought of as the total debt you owe compared to your total credit limit. You should aim to keep this number below 30 percent. The best credit scores have a credit utilization between 1 and 10 percent.

- Credit Age. Another factor in your credit score is the length or age of your credit history. This accounts for 15 percent of your score. Some lenders want to see the age of your oldest account; others want to see an average age of all of your open accounts. Either way, be sure to keep your oldest accounts open and in good standing.

- Different Types of Credit. Lenders want to see different types of credit on your credit report to demonstrate responsible behavior across a variety of accounts. While this may sound intimidating, there’s a good chance you already have different types of credit on your credit report — for instance, consumer credit cards, auto loans, or a student loan are different types of accounts. Different types of credit account for 10 percent of your Credit Score.

- Number of Inquiries. Lastly, the number of hard inquiries on your credit report can cause your score to drop slightly. Rounding out the last 10 percent of your score, while checking your credit yourself (a soft inquiry) won’t hurt your score, hard inquiries (such

as when you apply for a new credit card) will — so limit the number of new accounts that you apply for.

FICO Scoring Model Calculation (Weight) Factors

| Credit Factors | Credit Score Weight |

|---|---|

| Payment History | 35% |

| Credit Utilization | 30% |

| Credit Age | 15% |

| Different Types of Credit | 10% |

| Number of Inquiries | 10% |

Source: https://www.myfico.com/credit-education/whats-in-your-credit-score

All of these factors are considered when calculating your credit score. Some factors, ranked by their weight in the total score, count more than others. There are many different ways to improve your credit score, some of which can deliver rapid increases from 614 and some deliver results over longer periods of time.

What can you expect with a 614 credit score?

With a 614 credit score, while you are still considered to have Fair credit, there are plenty of lenders who will be willing to work with you, whether you are looking for a car, a house, or get a credit card. However, the chances are good that you will end up paying a bit more for the same items than would someone with a better credit score.

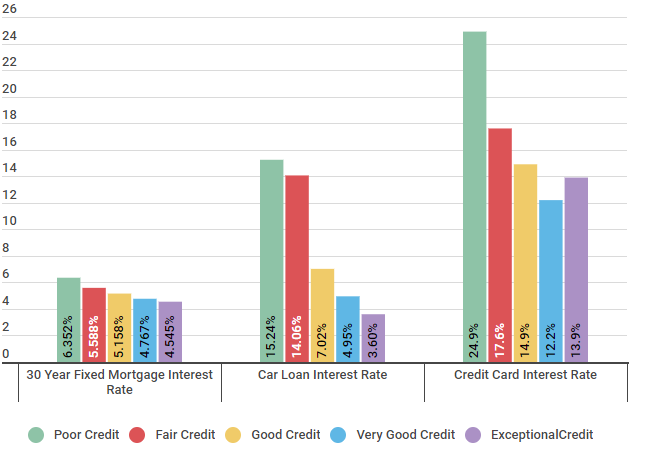

Here’s a quick breakdown of average interest rates for different credit score ranges on some of the most common purchases impacted by credit scores:

Interest Rate Ranges for Different Credit Score Ranks

| Type of Loan | Poor Credit | Fair Credit | Good Credit | Very Good Credit | Exceptional Credit |

|---|---|---|---|---|---|

| 30 Year Fixed Mortgage Interest Rate | 6.352% | 5.588% | 5.158% | 4.767% | 4.545% |

| Car Loan Interest Rate | 15.24% | 14.06% | 7.02% | 4.95% | 3.60% |

| Credit Card Interest Rate | 24.9% | 17.6% | 14.9% | 12.2% | 13.9% |

Source: Credit Sesame asked 400 members about their interest rates during a three week period beginning in January 18, 2018.

As you can see, you’ll end up paying a significant amount more in interest to purchase the same thing. For instance, the average credit card interest rate for someone with Fair credit is nearly 18 percent — this number is slashed quite a bit for someone with good credit.

Similarly, the interest rate on a car loan for someone with Fair credit can be upward of 14 percent — that number is closer to three percent with exceptional credit. In other words, it pays (literally) to try to improve your score.

Of course, there’s always room for improvement! If you’re not happy with your 614 credit score, one of the first (and best) things you can do is clear up any negative information on your report. Let’s learn some ways to do just that.

Dealing with negative information on your credit report

It’s no secret that negative information can have a huge impact on your credit score and your credit report. It will also affect your ability to get new credit with favorable terms in the future. Negative marks do not last forever. There are several things that can have a negative impact on your credit score:

- Chapter 7 bankruptcy stays on your credit report for 10 years

- Late payments or past due accounts stay on your credit report for 7 years

- Accounts that are sent to collections stay on your credit report for 7 years

- Chapter 13 bankruptcy stays on your credit report for 7 years

- Hard inquiries stay on your credit report for 2 years

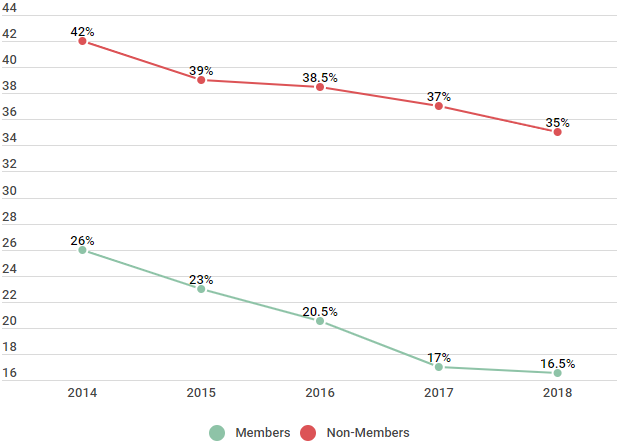

Research has shown many US consumers find their credit reports contain errors. Over time that number is decreasing, but with just under 17 percent of Credit Sesame members still finding errors as 2018, it is wise to stay vigilant.

Percentage of members and non members with inaccuracies on their credit report from 2014-2018

| Found Inaccuracies on Credit Report | Members | Non-Members |

|---|---|---|

| 2014 | 26% | 42% |

| 2015 | 23% | 39% |

| 2016 | 20.5% | 38.5% |

| 2017 | 17% | 37% |

| 2018 | 16.5% | 35% |

Source: Survey of 500 members and non-members who check their credit reports yearly. The survey was done in October annually.

The first step to improving your credit is to make sure that all the information on your current credit report is accurate. Next:

- File disputes for any inaccuracies; credit bureaus do not have to remove accurate information, nor are they likely to.

- Improve your previous negative habits and replace them with good habits. Bring any overdue accounts current, pay any liens (if necessary), work with collection agencies and creditors to clear up any collections, don’t apply for any new lines of credit, make sure to pay all of your bills on time, and pay down current debt asap.

Credit Report Inaccuracies, percentage resolved, and length until resolution

| Inaccuracies and resolution timeline | Members | Non-Members |

|---|---|---|

| Found Inaccuracies | 17% | 37% |

| Resolved Inaccuracies | 74% | 62% |

| Average Time for Credit to be Adjusted | <45 Days | 45-60 Days |

Source: Survey of 500 members and non-members who found inaccuracies on their credit report. Survey completed over the course of 9 months from December 1, 2017 – August 1, 2018.

The great thing about credit scores is that they’re not permanent — there’s always room for improvement. In fact, one of our Credit Sesame members had to improve her score to get the job that she wanted. Here is her story:

| Free credit score |

|---|

| What's a credit score |

| Building credit |

| How to increase your credit score |

| Average credit score by age |

| Whats the highest credit score |

Kyesia Had to Improve Her Fair Credit Score in 12 months to get the job she wanted

Member Since: 9/15/2017

| We interviewed Kyesia on September 25, 2018; she lives in Colorado Springs, Colo. and works at a local credit union as a teller making $26,000 a year. She is 25 and is engaged to her girlfriend of 5 years, Andrea. | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| What was your credit score when you first became a member? | |||||||||||||||

| My credit score was a 614, which doesn’t sound bad, but since I wanted to work at a local credit union, they require a higher credit score. They told me that it had to be in the “Very Good” range as per FICO scoring guidelines. It was a lot to process and thankfully I found Credit Sesame when I searched for help. | |||||||||||||||

| What | steps | did | you | take | to | improve | your | credit | score? | ||||||

| I really only did two things; made my payments on time and disputed all inaccuracies on my credit report. I got a part-time job working as a bartender at a local pub near our apartment so I had money always in my checking account. This way I could have automatic payments set up so I never forgot another one. Since I could walk to work we decided to sell one of our cars, clearing up not only a car payment but also the cost of insurance and gas. That savings also helped with making on-time payments. The other thing I did was dispute inaccuracies on my credit report. They had someone else’s social security number and their accounts on my credit report. It took a while to sort out everything, and my credit score actually dropped some when accounts were taken off. It took about 6 months for everything on my credit report to only reflect my actions. Once that was cleared up, all I did was made my payments and waited for the numbers to rise. | |||||||||||||||

| What | is | your | credit | score | now? | How | long | did | it | take | to | improve | your | credit | score? |

| My credit score is now 750. It has taken me a complete year to get where I needed to be. I finally got the credit union job I had wanted, and Andrea and I are looking at buying a cute 2 bedroom house. |

While not everyone is forced to improve their credit this quickly, Kyesia shows that it can be done. Using the tips that Credit Sesame has available, Kyesia was able to not only increase her score but to get the job that she had really wanted.

TLDR; what can you do with a 614 credit score?

While a 614 credit score certainly isn’t the best score you can have, you still have plenty of options when it comes to your credit (even though you may have to pay a bit more for them). The best thing you can do is to take the proper steps to work to improve your score.

The good news? Time, along with the proper steps and action, can improve even the lowest credit score. The impact of the negative factors on your score lessens, and the negative marks will eventually fall off completely — leaving you with a higher score. While you’re waiting, good credit habits will help you build positive credit. These behaviors today mean that when the negative reports cycle off of your credit report in the future, you’re left with a better score.