Credit Sesame discusses housing insecurity and how it affects Americans of different genders and income levels.

Inflation has left its mark on household budgets around the country. It’s especially tough when fast-rising prices hit one of the most basic needs: shelter.

As fast as inflation has been rising, the cost of rents has been rising even faster. Combined with the general rise in household expenses, this contributes to the problem of housing insecurity.

While housing insecurity is a problem across the country, it affects some segments of society more than others. A new Credit Sesame study looks at the current state of housing and who is most affected.

What is housing insecurity?

Housing insecurity is the risk of losing your home. This usually means being evicted from a rental property or foreclosing your house. Those two types of housing insecurity have in common that they can both result from failing to keep up with your rent or mortgage payments.

Renters are generally much more exposed than owners. Homeowners tend to be more wealthy than renters, and their housing costs are usually more stable.

After all, while housing prices have risen sharply in recent years, once you buy a house, you’ve locked in the purchase price. Also, most mortgages have fixed interest rates, so rising rates don’t typically affect payments.

On the other hand, renters can see their housing costs rise from lease to lease. They are also more vulnerable to being forced to leave a property and find another place to live.

Measuring housing insecurity

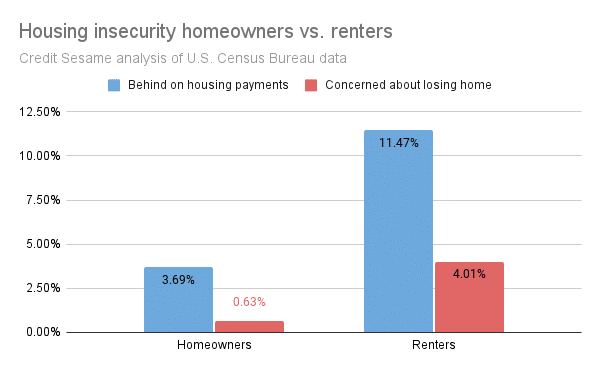

Credit Sesame analyzed data from the Census Bureau’s Household Pulse Survey to measure household insecurity earlier this year. Part of that survey estimates how many renters and homeowners are behind on their rent or mortgage payments. It also asks renters how likely they are to have to leave their homes due to eviction within the next two months. Similarly, the survey asks homeowners how likely they are to have to leave their homes due to foreclosure within the next two months. As expected, the survey shows that the issue is a much bigger concern for renters than homeowners.

As the above chart shows, renters are much more likely to be behind on rent payments than homeowners are to be behind on mortgage payments. Not surprisingly, a higher percentage of renters said they were very or somewhat likely to lose their homes within the next two months.

Since the issue is much bigger with renters than homeowners, Credit Sesame focused its examination on renters.

Recent trends in housing insecurity

Although the economy has grown and unemployment is very low, high inflation might affect housing security.

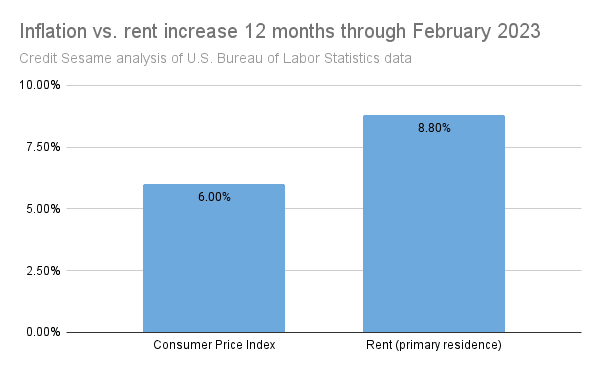

Not only do rising prices make it more difficult for households to keep up with their bills, but according to figures from the Bureau of Labor Statistics, rents have risen even faster than inflation in general:

This increases the risk of housing insecurity. A closer look at the numbers shows how this risk affects different American groups

Housing insecurity hits hardest in middle age

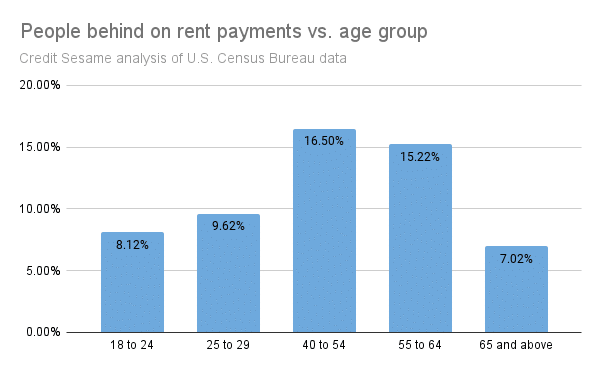

As many financial challenges as young adults face, the problem of housing insecurity seems to hit middle-aged adults the hardest:

The percentage of people behind on their rent payments peaks in the 40 to 54 age group. It is almost as high in the 55 to 64 age group. In contrast, the oldest and youngest adult age groups have the two lowest percentages of people behind on rent payments.

The surge in delinquent rents among middle-aged adults may be because older people are more likely to support families and thus have greater financial responsibilities. It should also be noted that the number of renters drops sharply after age 40. Since higher earners are more likely to become homeowners, there is a good chance that older renters are often in lower-income groups. As you might expect, there is a strong relationship between income and housing insecurity.

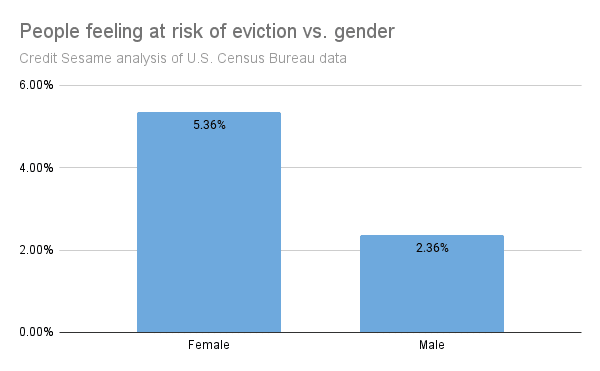

Women feel more housing insecurity than men

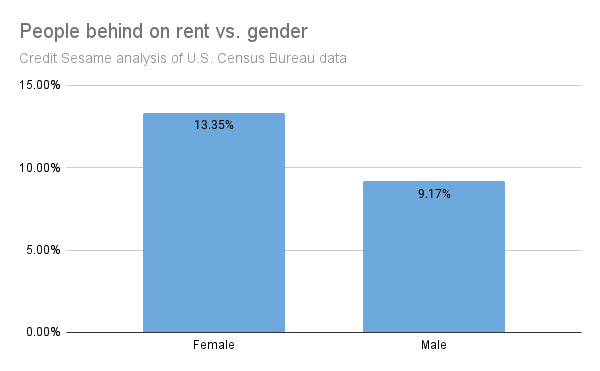

Breaking the numbers down by gender revealed a higher degree of housing insecurity among women than among men:

First, more women than men are behind on their rent. Not surprisingly, women are more likely to say they are very or somewhat at risk of being evicted within the next two months:

One reason why women may be more subject to housing insecurity is that women typically make less money than men. Again, income is a huge factor in housing insecurity.

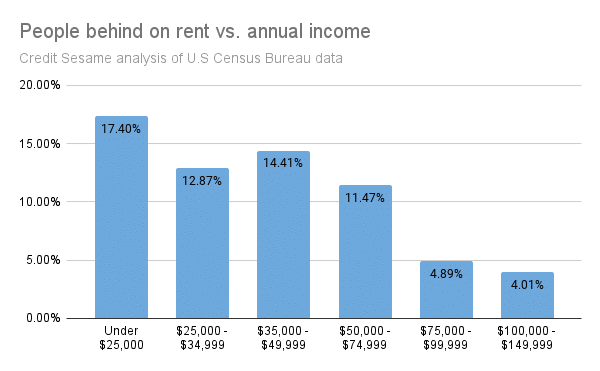

Housing insecurity is very income-driven

It is no surprise that the poorest Americans are most likely to be behind on their rent payments. The following chart shows how being behind on the rent corresponds with income level:

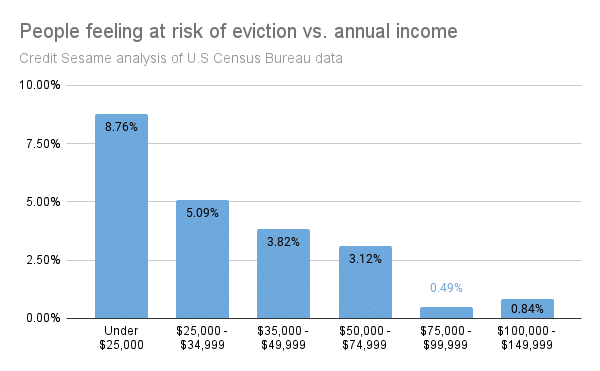

Lower earners are also much more likely to say they are either very or somewhat at risk of eviction during the next two months:

Again, it’s no surprise that the less you earn, the harder it is to pay the rent. As long as high inflation continues, rental inflation and insecurity among lower earners are likely to remain high.

The growing problem of housing insecurity

The figures show that housing insecurity is already a serious problem, especially for specific population segments.

High inflation certainly doesn’t help, and the problem might worsen if a recession puts more people out of work. The possible resumption of student loan payments later this year is another factor that might make it even more challenging to come up with monthly rent payments.

The best response is for households to tighten their budgets and rein in their use of debt. That’s never easy, but it’s worth the effort when the roof over your head may be at risk.

If you enjoyed Housing insecurity hits Americans unevenly you may like,

Disclaimer: The article and information provided here is for informational purposes only and is not intended as a substitute for professional advice.