Credit Sesame explains how credit card companies may restrict access to credit when you need it most.

Besides inflation, higher interest rates and a slowing economy, consumers have something else to worry about this year.

Credit card companies may start restricting access to credit just as you need it the most. That puts consumers and credit card companies on a collision course. This article explains why that is and how you can avoid the collision.

Credit card companies are freezing and limiting credit

It helps to understand how credit card companies can manipulate your access to credit via a credit freeze or the extent of your credit limit.

Credit freezes for gas purchases have risen

A credit freeze occurs when you use a credit card for a purchase, but it’s not yet clear how much that purchase will cost. To make sure there’s enough money available for the purchase, either the merchant or the credit card company may put a temporary freeze on part of your credit.

That means they lock up a high-side estimate of what it will cost. Once the final amount is known, that amount is charged to your account and any remainder is unfrozen.

You may have experienced something like this when checking into a hotel or renting a car. Your credit card is used to secure any expenses you may incur during your stay or damage you may cause to the vehicle during rental. Since the possible future expense amount is unknown, a portion of your credit limit might be frozen so it’s available in the event it is needed. That portion of your credit limit would be unavailable to you until the freeze is lifted.

Something similar happens when you use your credit card to buy gasoline. When your card is used at the pump to authorize a purchase, the amount of that purchase isn’t known yet. So, a freeze is put on your credit limit large enough to cover that purchase. It can take a day or so before that freeze is lifted.

In response to rising gas prices, Visa and Mastercard have increased the amount of credit they freeze for gas purchases from $125 to $175. This is a 40% increase and means you have a lot less credit available than previously.

Some credit limits may be cut as the economy slows

Economic conditions may prompt your credit card company to reduce your credit limit.

When the economy gets weaker, it becomes riskier to extend credit. This may result in credit card companies lowering the credit limits for some customers.

A recent study by the Consumer Finance Protection Bureau (CFPB) looked at how credit card companies managed credit limits during the two most recent recessions. The CFPB found that reductions in credit limits were common during those periods.

The study found that two-thirds of those reductions occurred even though the customer had no recent history of missing payments. That means your credit limit could get cut even if you haven’t done anything wrong.

The U.S. economy shrank in the first quarter of 2022, and there is widespread concern that it might be headed for a recession. If that happens, you may find yourself with less credit available than you thought.

Consumers using more credit

Credit freezes and cuts to credit limits reduce consumers’ access to credit. This could happen just as people are relying more on their credit cards.

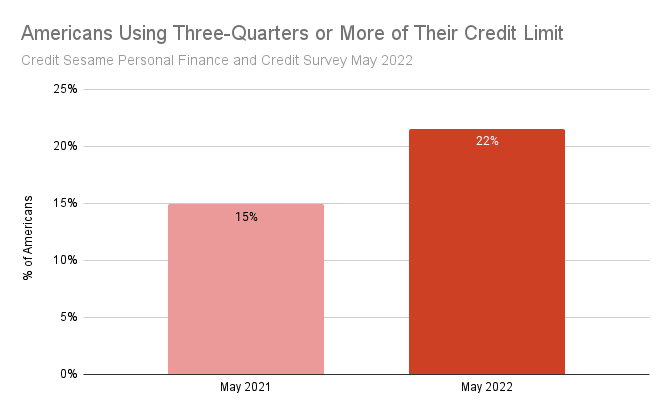

A recent Credit Sesame survey found that the percentage of credit card customers using at least three-quarters of their credit limit has jumped this year:

More people are running close to the limit on their credit cards this year. At the same time, credit card companies have increased credit freezes and may start reducing credit limits.

That’s why credit card companies and their customers are on a collision course.

Impact on consumers

The combination of these trends could impact consumers in three important ways:

- Credit available may be more limited. You may be counting on that credit to help see you through tough times. Unfortunately, a combination of higher credit freezes and lower credit limits may give you less credit to lean on.

- Available credit should be monitored. You may never have exceeded your credit limit before but that could change. Since there may be less available than you’re used to, make sure you regularly check how much is left.

- Credit score go down. Higher credit freezes and lower limits could cause you to use a higher percentage of your available credit. That percentage is known as credit utilization, and a higher rate of credit utilization can hurt your credit score.

Adjusting your credit use

Given these conditions, there are three things you should consider doing to make sure your credit is available when you need it:

- Limit credit card spending. Tightening up your budget is always a good idea in a shaky economy. Plus, cutting back on credit card use is a good strategy when interest rates are rising.

- Pay down balances sooner. With the possibility of credit limits being cut, make it a priority to pay down balances as fast as possible. This helps your credit score by limiting credit utilization. It also keeps some of your credit limit available for when you really need it.

- Shop for better terms. Between rising interest rates and the possibility of credit limits being lowered, this may be a good time to shop for a new credit card with better terms. Plan carefully though, because opening too many credit accounts at one time can hurt your credit score.

Navigating to avoid the collision is tricky, but may be necessary to preserve your credit. As a side benefit, these same moves should also reduce your exposure to this year’s rising interest rates.

You may also be interested in:

- Maximize Your Credit Card Payments to Minimize Your Costs

- Record Credit Card Use in March 2022 Comes at the Wrong Time

Disclaimer: The article and information provided here is for informational purposes only and is not intended as a substitute for professional advice.

Survey methodology

The Credit Sesame Personal Finance and Credit Survey 2022 was designed and executed by Credit Sesame using the Momentive Inc. survey tool. General population data was collected online May 20-21, 2022. The survey sample comprised 1,222 U.S. residents aged 18 to 99 years balanced for age and gender using U.S. Census data. The sample data is accurate to within + 2.88 percentage points using a 95% confidence level.