Independence. That means not dependent, right? When we carry debt, we are beholden to creditors (almost always at a cost) and never truly financially independent. We depend on getting our hands on enough money every month to pay those creditors.

Independence from credit card debt is something we’d all like to have. Yet, among Credit Sesame members who have credit cards, a shocking 91% still carry a balance at the end of the month. These members carry an average balance of $4,386.

This made us wonder: what does life look like on the other side? How does being credit-card-debt-free affect the other 9%? Do trumpeting angels and pink unicorns follow these hallowed people around all day?

We examined the data to find out (about their wallets, at least—it’s your guess what the trumpeting angels and unicorns do).

No credit card debt = better credit scores

The average credit score for members with no credit card debt is 709.

Among members with credit card debt: 640.

These 69 points might not seem alarming, but this credit score range makes a world of difference. It’s the difference between poor credit and good credit.

People who carry credit card debt have higher credit utilization ratios — the percentage of their credit limits they’re using. People with no credit card debt have a credit utilization ratio of 0%. Among members with credit card debt, however, average utilization shoots up to 35%. Utilization has a huge effect on your credit score, second only to payment history.

Furthermore, credit card debt is a sign that a consumer might not be on the best financial footing.

High credit scores don’t guarantee financial confidence

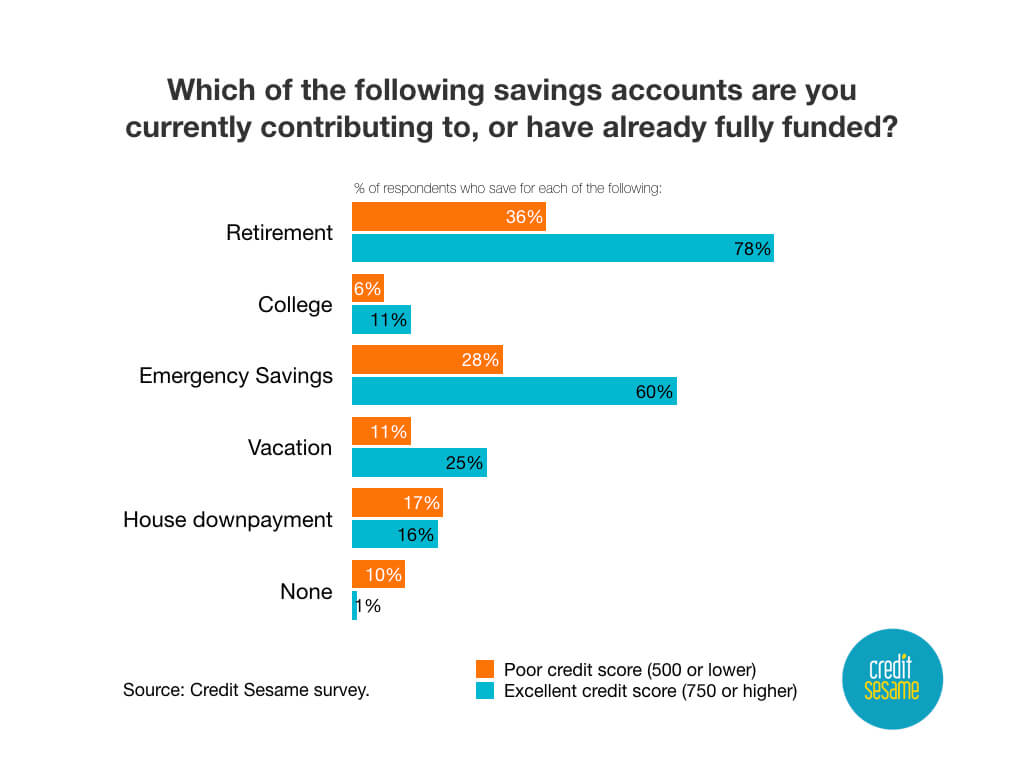

We also surveyed 1,018 Credit Sesame members with credit scores of 750 or higher and those with poor credit scores of 500 and lower.

The good news is that 78 percent of respondents are actively saving toward retirement. This probably indicates a high percentage of people whose employers offer 401(k) plans that employees can contribute to by paycheck deduction. Automatic savings are the easiest to maintain.

For those with poor scores, one in 10 of people said they are not saving at all.

The bad news is that only 60 percent are saving toward or have fully funded their emergency fund. Emergency savings are critical for handling financial crises that arise in life (and they always do).

A little more bad news: only 11 percent are saving a college fund. With seven million U.S. consumers in default on their student loans, we think having a solid plan for funding an education is critical to financial and credit success.

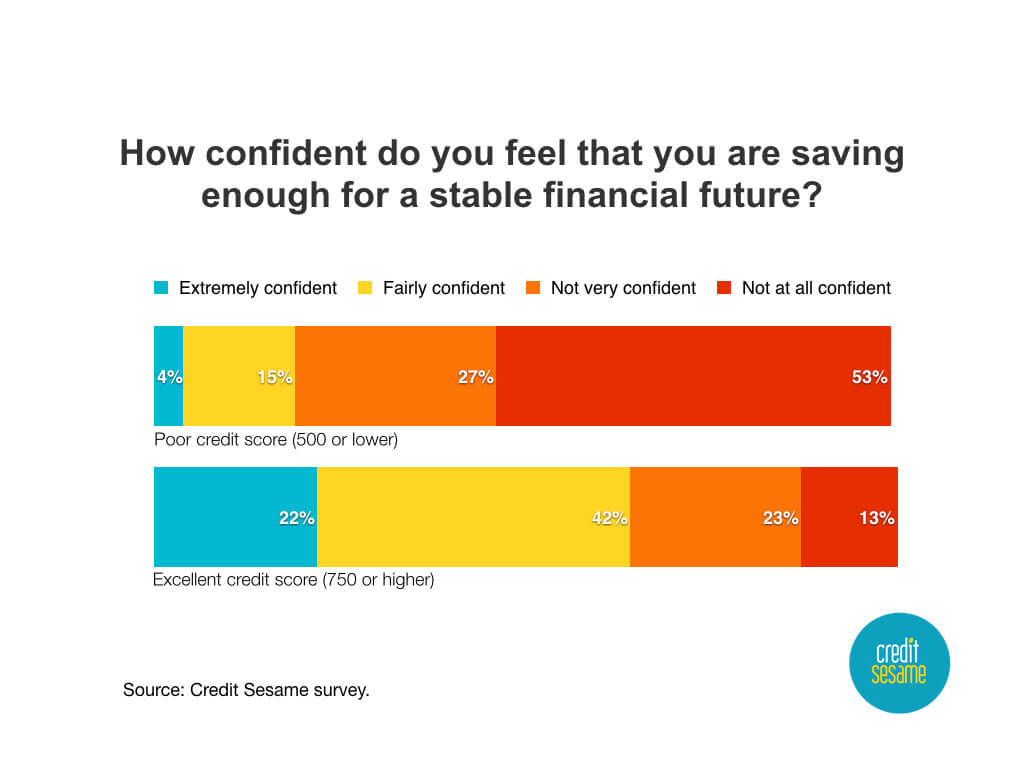

What we discovered is that high credit scores don’t necessarily indicate true financial independence or a high level of confidence in a consumer’s financial future.

In fact, the key indicator of financial confidence is savings.

Active saving = higher confidence in financial future

We see a direct correlation between Credit Sesame members with excellent credit scores who actively save toward their goals or who have fully funded those goals and the confidence they have in their financial future.

Members who are not currently saving toward retirement, college, an emergency fund or a vacation fund have the lowest confidence of all.

| Below: Which of the following are you currently saving for, or have you already funded? | Extremely confident | Fairly confident | Not very confident | Not at all confident |

|---|---|---|---|---|

| 22% of respondents with excellent credit scores | 42% of respondents with excellent credit scores | 23% of respondents with excellent credit scores | 13% of respondents with excellent credit scores | |

| Retirement | 87% | 86% | 80% | 32% |

| College savings | 20% | 12% | 7% | 0% |

| Emergency Savings Account | 63% | 62% | 62% | 48% |

| Vacation savings | 36% | 26% | 21% | 5% |

Avoiding debt, funding an emergency account, and saving toward known future financial needs are behaviors that clearly lead to financial peace and freedom.

No credit card debt = higher credit limits

You’d think that people who have credit card debt would be more likely to have larger credit limits, right? Wrong.

Paradoxically, people with no credit card debt have higher credit limits. The average credit-card-debt-free person has a total credit limit of $12,473, spread across two cards. On the flipside, people with credit card debt have a total credit limit of just $9,405, spread across three cards.

What causes this weird phenomenon?

As we just saw, people with no credit card debt have higher credit scores, on average. They get these high scores by using credit cards wisely. This raises their score, and they are rewarded with higher limits on existing cards and higher limits on new cards for which they apply.

Men have similar balances but higher credit limits than women

Turns out men generally achieve lower utilization ratios and therefore higher average credit scores than women. Here’s how.

On the surface, men and women appear equal in terms of credit card debt. They have nearly equal average credit card debt. That’s where the similarities end, though.

- Men are given more total credit than women. Men are more likely to have higher credit limits for each card.

- Men have more cards than women. The average indebted dude has one more credit card than our average indebted lady.

As a result, indebted men have $4,500 more total available credit than indebted women.

With the same average debt, the guys’ utilization is lower, and that’s better for their credit scores. Ten percent lower, to be specific. That’s a huge setback to the credit scores of the ladies.

Why? One reason could be women’s lower average incomes. Also, they have significantly more student loan debt. These factors could make men look like better borrowers.

Of course, it’s still possible for women to overcome these barriers to excellent credit. They just have to work harder to achieve the same score.

No credit card debt = less overall debt

Having credit card debt doesn’t cause you to have other kinds of debts, but it does indicate the likely presence of a trend or pattern.

Among people who do have other types of debt, the total amount owed is far less for people with no credit card debt. Take a look.

| People With Credit Card Debt | People Without Credit Card Debt | Percent Difference | |

|---|---|---|---|

| Mortgage | $198,264 | $179,065 | 11% |

| Home Equity Loan | $54,013 | $45,637 | 18% |

| Auto Loans | $19,932 | $15,305 | 30% |

| Student Loans | $38,194 | $25,118 | 52% |

| Unsecured Loan | $7,023 | $2,986 | 135% |

It’s possible that people who are already credit-card-debt-free are debt-averse and have either moved on to paying off their other debts, and/or avoid taking out more debt in the first place.

Is credit card debt a good measure of financial health?

Don’t focus on one-track measures of financial success. Absence of credit card debt is an important indicator of your financial health, but it’s just one small slice of a very complicated cake.

Don’t focus on one-track measures of financial success. Absence of credit card debt is an important indicator of your financial health, but it’s just one small slice of a very complicated cake.

Look at the bigger picture. Do you save enough for retirement? Do you work to pay down other debts? Do you have a sufficient emergency fund? All of these things—and more—contribute to a well-rounded financially healthy person.

At the same time, don’t poo-poo credit card debt and its significance. The numbers clearly show that it correlates with all other sorts of other measures of financial health, like overall debt levels, credit scores and credit limits

Just as your weight is only one (very important) measure of your overall physical health, credit card independence is one (very important) measure of your overall financial health.

Methodology

We surveyed a total of 1,028 Credit Sesame members. Specifically, we surveyed 591 members whose credit scores were 750 or higher, and 427 members whose scores were 500 or lower.