Credit Sesame explains how borrowing can make the inflation problem even worse.

Consumers are feeling the pinch of rising prices. With inflation at its highest level in over 40 years, paychecks don’t go as far.

A recent Credit Sesame survey found that as wages come up short, Americans are relying on their credit cards to make up the gap. That may be the wrong solution.

This article looks at how borrowing can make the inflation problem worse. It also suggests steps you can take to reduce borrowing costs so you don’t add to the higher prices you’re paying.

Inflation is leading Americans to borrow more

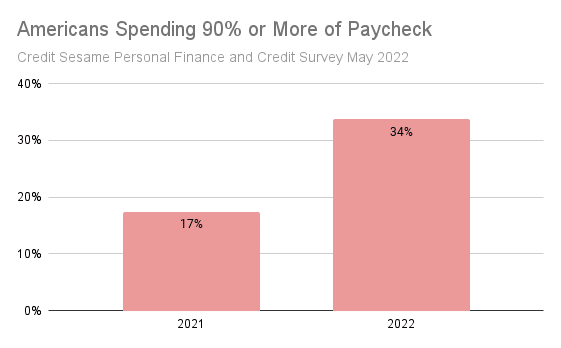

The Credit Sesame survey found that wages are having a hard time covering routine expenses. More Americans are having to spend 90% or more of their paychecks every week:

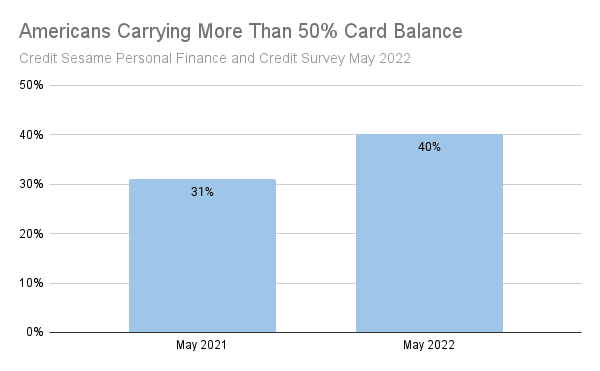

Some people are responding by using their credit cards to make up the shortfall. As a result, credit card balances have been rising:

Given the way high inflation has consumers by surprise, it’s understandable that so many have turned to the most convenient solution at hand – their credit cards. However, as high inflation persists, this may not be the best solution.

How credit card borrowing compounds the inflation problem

While increased credit card borrowing may be a response to inflation, it can also add to the problem in a couple ways:

- With more people carrying credit card balances this year, they face paying interest charges on top of their purchase prices.

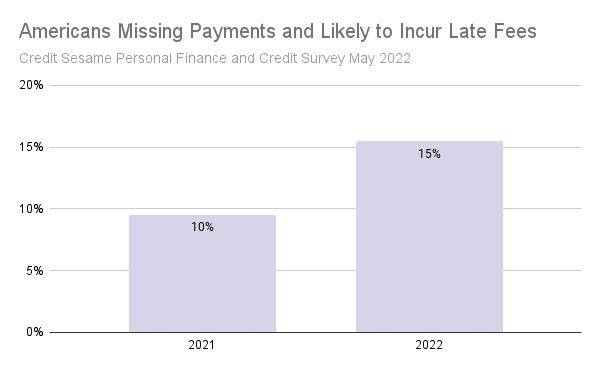

- As shown in the chart below, more people are missing payment due dates. When this happens, late fees can add to the expense.

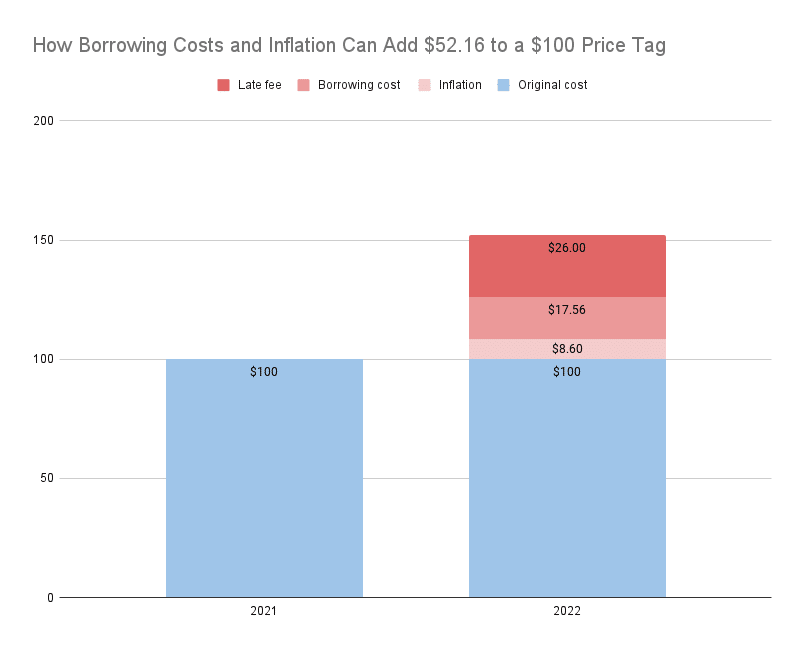

When you add up how much all this could add to a purchase that cost $100 last year, the results are shocking. Inflation is up 8.6%. According to the Federal Reserve, the average interest rate charged on credit cards is 16.17%. Finally, the Consumer Finance Protection Bureau (CFPB) has found that the average late fee on general purpose credit cards is $26 for a first-time occurrence.

Here’s how all that stacks up if you carry that credit card purchase on your balance for a year, and are late with a payment at some point:

Based on recent inflation and borrowing habits, a combination of higher prices, interest charges and a late fee could add $52.16 to what was a $100 purchase last year.

An 8.6% inflation rate is bad enough. In the above scenario, you’d be looking at a 52.16% total increase in costs.

If that seems like an extreme example, keep in mind that interest rates are on the rise, so that expense might be getting worse. Also, the late fee used in example was for a one-time, first-time occurrence. The CFPB found the average late fee for repeat occurrences is $35, so missing more than one payment could add to the damage substantially.

To avoid having borrowing ramp up the toll inflation is taking, you may need to adjust some of your financial habits.

Credit cards are not meant for long-term borrowing

For starters, credit cards are great for the convenience of acting as a cash alternative. If you pay your balance off in full each month, this can be a cost-free service.

However, credit cards are a bad choice for long-term borrowing. Their interest rates are much higher than alternatives like personal loans and home equity.

So, think before you use your credit card. If you’re not going to be able to pay off the charge fairly soon, you might be better off finding another means of borrowing.

Rethink your budget to account for inflation

Of course, another alternative to borrowing is to forgo some purchases. The simple truth is that inflation may mean you can no longer afford to buy as much as you used to.

Take a fresh look at your budget in light of current prices. Figure out how much still fits your current income, and decide what stays and what goes.

This isn’t pleasant, but the more of your income is going to pay borrowing costs, the tougher these choices will become.

Plan your borrowing to minimize costs

Just because interest rates are rising doesn’t mean you have to stop borrowing. Using credit may still be essential for convenience and to make long-term purchases affordable.

What rising rates do mean is that you need to plan your borrowing carefully. As credit gets more expensive, it needs to be viewed more as a limited resource. You have to use it where it’s most important.

Start by considering the forms of credit available to you:

- Secured loans, like mortgages and car loans are generally the cheapest. Use these where possible. If you have equity in your home, that can be a valuable resource for making other purchases more cost-effective. Just remember that a secured loan means you’re using a valuable possession like your house or your car to guarantee repayment.

- Personal loans may be unsecured, but they are generally a lot cheaper than credit card debt. Plus their more structured repayment schedule can help you plan for how quickly you’ll pay off the debt and how much interest it will cost you. In order to keep debt from snowballing, it’s best to save personal loans for purchases whose use will outlive the term of the loan.

- Credit card debt. As discussed earlier, credit cards should be used more for short-term convenience than for extended borrowing. Avoid using a credit card just because you can’t figure out any other way to pay. You should be budgeting your credit card use, and that budget should include a plan for how to pay it off within a month or two.

Compare credit card rates

When you use your credit card, make sure you’re using the most cost effective one.

Not only do credit card rates vary a great deal, but in today’s economy those rates may be changing quickly.

So, take a fresh look at your existing cards to see which offers the best interest rate. Also, keep an eye out for credit card offers that feature a better rate.

Consider consolidating current credit card debt

If you have credit card balances you can’t pay off right away, at least see if it can be refinanced or consolidated into a more cost-effective form of credit.

Home equity loans, personal loans and balance transfer credit cards are among the things you might be able to use to consolidate or refinance existing debt at a cheaper rate. Just be sure you have a repayment plan before you commit to any new debt.

Recent inflation is at a level that hasn’t been seen for over 40 years. That makes this economy something very different from what consumers have gotten used to.

To adapt successfully, you need to rethink your spending and credit habits. The ideas discussed in this article should give you some thoughts to consider.

You may also be interested in:

- Recession and Inflation as Threats to Personal Finances: Which is worst?

- Highest Inflation Since 1981: What Does This Mean for the People of America?

Disclaimer: The article and information provided here is for informational purposes only and is not intended as a substitute for professional advice.